Studies of heating systems. Russian heating equipment market: current status and prospects

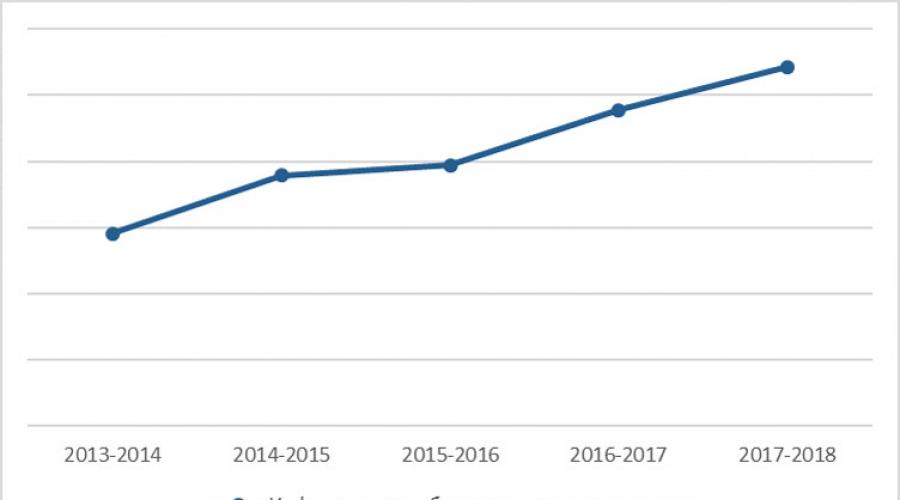

The inverse tendency is observed by the popularity of which to the current winter decreased compared to 2014-2015 more than 3 times. By the way, it was the electrocheamins that were leaders in the demand of winter 2013-2014! Similar dynamics and water heaters: a small rise in 2014-2015, and then a protracted decline.

It should be noted that in this winter the popularity of energy-efficient solutions has increased, among which from the top 30 of our catalog we have taken already mentioned heat accumulators, indirect heating and electric.

Analysis of demand for major cities

We calculated the top 15 cities in the number of ways of their inhabitants in the hardware directory of the portal site. The picture turned out curious. First, 13 out of 15 "top" cities have increased their interest in heating technology. The decline was shown only St. Petersburg and Samara. Interestingly, Minsk entered the TOP-15, ahead of many Russian millionth citys. Note that the number of goals to the equipment catalog from Moscow almost doubled this value for St. Petersburg, which, in turn, is 1.5 times ahead of Krasnodar.

By the way, we did not take into account the goals from the Moscow and Leningrad region, otherwise this gap would be even more noticeable.

Nevertheless, the total number of goals to the catalog is not as indicative as interest in certain categories of equipment in the context of cities. We decided to analyze the demand for heating boilers in different cities. To begin with, a consolidated demand diagram on the 6 most popular categories of boilers in the last two winters.

they produce heat, pipes are delivered to the consumer - radiators. There are still pumps, valves, expansion tanks and other network equipment, but these three segments are fundamentally important in heating systems. If you measure these markets in money, then their volume in the final retail prices is very similar. Each of the three segments of the heating market at the end of 2015 is located in 1 billion dollars.Anton Tamakov, Deputy Director "Litvinchuk Marketing"

Overview of the market of water heating systems from Litvinchuk Marketing.

As for the dynamics of markets, in 2015, with a quantitative measurement in all three segments, it turned out to be negative. In 2015, compared with 2014, the boiler market fell by 19%, the market of pipes and radiators asked 16%. "Made in Russia" the proportion of Russian products is very different in all three segments.

Inside the markets of radiators, pipes and boilers there are segments with a high proportion of domestic products. For example, in the market of pressure pipes, the segment of polypropylene pipes by more than 50% consists of products produced in Russia.

In the segment of boiler equipment, industrial boilers are more than 50% of the Russian assembly. In heating radiators, the segment of convectors is most imported.

Market trends

At the end of 2015, the market in quantities asked 16%, in money (when calculating in EUR) - by 23%. The reason for the disproportion is in the substantial growth of the segment "Super Economy" against the background of a sharp drop in the share of European radiators. At the same time, the year was marked by a significant decrease in the trading charge at all levels of the distribution system - ranging from manufacturers and ending with end vendors.

If we consider steel panel radiators, last year the factory prices have decreased on them, however, it has nothing to relate to the weakening of the ruble - the world's steel prices have gradually decreased over the past three years. As for segments with high added value (for example, steel tubular and design radiators, expensive convectors), then their cost currency exchange rates are much stronger than the price of metal. For most positions, the courses are fixed at the time of the conclusion of contracts.

The psychology of consumer behavior was very much changed after the crisis of 2009. Now the buyer's choice is increasingly stopped at an inexpensive product, the economy segment is actively growing. Premium consumption at the same time is quite stable, and if it changes, then much less pace.

The rapid growth of the "lightweight" aluminum radiators segment is one of the evidence of such an assumption. Already in 2014, the main market segments stopped growing and outlined negative dynamics, in 2015 this trend continued its development. The reasons for this situation are several.

First, the general state of the Russian economy and a significant drop in the purchasing power of the population began at the end of 2014. Even record housing entry rates (81.3 million square meters of living space in 2014 and 81.5 - in 2015, against 70.5 million square meters in 2013) did not help.

Secondly, sales in the secondary market show all signs of saturation. Sales of replacement radiators that have reached the peak in 2012-2013 (up to 70% of all sales), already in 2014 went to the decline. In 2015, the expected reduction in this segment occurred. The fact is that people with a high and middle taste in their mass have long changed outdated and unaesthetic devices to more modern. And those who received (and gets) low incomes, in 2015 it was not prior to replacing radiators.

According to our estimates, over the past 10 years, it has been replaced from 58 to 65% of all heating devices, that is, their flesh is very fresh. Therefore, the amount of replacements should have been drastically reduced in the coming years even without the participation of the crisis. It can be said that the crisis will make this process smoother and less painful. At the same time, the fall affects, first of all, the market of aluminum and bimetallic radiators, which were mainly used to replace old cast-iron "batteries" and convectors.

It can be predicted that for the 2015-2017 the replacement market will decrease by 40-50%, and the sales market in new construction - by 20-25%. Moreover, in 2016, the radiators market waits for a reduction by 25%. At the same time, the panel-type instrument market (they go to the new buildings by 90%), it is unlikely to decrease by more than 10-15%, and expensive design radiators going to elite housing are practically not affected.

The volume of the PGO market has a pronounced seasonality. The market capacity changes twice, increasing in the peak of seasonal demand (August - October) to 170-175 million rubles per month, and falling in the spring (March-April) to 85-90 million rubles per month. At the same time, there is a tendency towards constant growth, over the past years, the market increases by about 13-18% per year. A characteristic feature of the market is a small number of large end consumers. The amount of average application ("average check") is 50-60 thousand rubles, which corresponds to 1500-1700 transactions per month in April-May and 2800-3400 in September-October. It should be noted a sharp decrease in the size of the average application in February-March to 25-30 thousand rubles. This is due to the fact that during this period, equipment for new construction is usually not purchased. Only individual units of equipment for reconstruction (replacement) of the existing one are purchased.

PGO is heterogeneous: the market consists of several practically not competing segments. Competition occurs within the data segments among substitute goods (substitutes) manufactured by various manufacturers. On average (there are differences between segments) The product enters the final buyer through a chain of 2 intermediaries. Directly from the factories to end users without intermediaries is sold about 18-20% of the entire equipment produced. This allows us to conclude a large value for the market of trading organizations, since the main volume of purchase and sale operations produce exactly they. It should be noted that we are talking about the averaged data, some manufacturers have a different situation.

For example, the sales system of the plant "Glory and Hope - Gas" producing a grip * is aimed at establishing direct contacts with end users, bypassing intermediaries. The advertising company is aimed at creating a positive image of the company in the business community, strengthening the recognition of the brand, the popularization of produced products among consumers. Currently, the sales of "SIN-GAS" among competitors producing hydraulic fractures are small - about 1%. However, due to the fact that the plant is taken for the manufacture of any, even the most non-standard, orders, it is likely that the market share occupied.

The enterprise "Center for Innovative Technologies", which produces a gas control system, from 90 to 100% produced products buy intermediaries. This is due to the policies of the sales policy, as well as by the lowest fame of the manufacturer's name to end consumers. Basically, the produced products are advertised - the system of automatic control of SACZ gas. Since competitors do not produce products with the same name, all orders through one or another chain intermediaries are placed directly on the manufacturer. There is a danger: in case of the emergence of any competitor who uses this name for its product, the company's share in the security system market (currently about 25%) will be instantly "blurred." As practice shows, the current legislation is not able to effectively regulate the issues of copyright and related rights, which makes it impossible (or very difficult) upholding its legitimate interests in the event of such situations.

The signal "Signal" (Engels) has begun to serial production of GRPS in the fall of 2002. Until this time, the "signal" produced only the regulators, and the grip produced Radon. However, the "signal" for a long time sold them under its brand. The overwhelming majority of consumers did not even guess that the grip produces another plant. When the "signal" opened its own production, he began to produce the same grip under the same trademark. After the "signal" launched the production of the grip in the series, he pulled Radon to the price war, which took place from November 2002 to February 2003. All these actions helped the "signal" in a short time to change the placement of forces among manufacturers and capture 10% of the grip market. Today, produced by Radon and the "Signal" of GRPS are the most popular on the market, and their price is the most acceptable to the consumer.

Often, consumers do not have the ability to use the fruits of such competition. The situation with the "Center for Innovative Technologies", described above, is precisely those when competition does not reach the consumer. It is almost completed at the design stage: the product that the designer has included in the project has a very strong advantage over substitutes. Often, the person responsible for the complete set does not even suspect the presence of substitute goods that have a different name. At the factory producing any product, also in very rare cases may provide information from this kind. The reasons for that two. The first banal: Thus, there will be an indirect advertising of a competitor with the Customer's redirection, which no self-respecting manufacturer can admit. The second reason is not so simple. According to a marketing research conducted by the Independent Research Center "Miomark", public opinion is posing technical training of staff of manufacturers of the PGO significantly higher training of personnel trading organizations. In practice, the preparation of the governing composition at the factories and the discoverships is approximately the same, and the literacy of ordinary engineers, as the study showed, directly depends on the salary obtained by them. But during the study, an important detail was found to: all workers checked for technical literacy can show it only in relation to the equipment with which they are constantly dealing. And here it affects the lack of producers wide outlook. Since when performing the usual circle of duties, factory workers are usually encountered only with the products of their factory, often it is simply nothing known about the products produced by competitors. It turned out the most interesting thing: only 20% of producers of the PGO are interested in the development of competitors! If in European countries, the monitoring program of competitors (industrial espionage) is the most important part of the marketing activities of enterprises, the lack of tough competition in Russia gives manufacturers the opportunity not to engage in this activity at all. It looks especially strange in the segment where competition is present and takes enough hard forms. We are talking about the production of grip.

Although CRPS currently is produced in Russia with a large number of manufacturers, serious players in this market are not so much. There are the following approaches to the production of GRPS: vertical production - when the plant fully manufactures all equipment and all the reinforcements that are part of the product, and assembly production - when equipment and fittings are purchased from other manufacturers. Combined production - when part of the equipment is made altogether, part is purchased on the side - is currently not practiced. Today, a vertical approach to the production of hydraulic grip is carried out at the "Signal" factories, Gazazpararat and Gazprommash. It also applies to the Saratov enterprise "Ex-form", the release of small batches of promising cabinet installations of UGRS-50 with a direct-flow regulator of the RDP.

A vertical approach to production has a significant plus: independence from sediments. All other Russian manufacturers practice assembly production, the main plus of which is the ability to focus on the same operation: installation of technological equipment in the closet. The undoubted leader of the assembly production is Radon, Engels. All other manufacturers either work on local markets, or the volume of products produced does not have a significant impact on the Russian market. However, within the local market, the position of such a regional producer can be quite durable ("Gasomplekt", Reutov, Cambarian Gas Equipment Plant, etc.).

The graphs are visible in April 2003. Prices for the most popular grip model - with a regulator of RDNA 400-01 or analogue. You should immediately make several comments to the above graphics.

The recognized center of the production of industrial gas equipment is definitely a Saratov should be recognized. In Saratov and Engels (satellite city), according to various estimates, produced from 67 to 75% of the entire equipment produced in the country. The average price of GRPS 400-01 - from 17 to 18 thousand rubles. The high price of the grip plant Gazprommash is due to the fact that it works primarily on regional markets, in particular all Tyumen companies (Angor, Gazstroyinter and Interregional) offer cabinets of Gazprommash. This cabinet is produced both with a standard RDNA-400 regulator of the "signal" and the Gazprommash regulator of the RDNA 50/400, having a slightly smaller bandwidth. The relatively low price of GRPS, made at the Gas Equipment Plant, Kazan, is due to the small fame of this manufacturer and the smaller value of the materials used by the plant for production. Despite this, the price / quality indicators for these products are quite acceptable, which is confirmed by the steady increase in sales. Trading organizations of the city of Kazan, shown in charts ("Komtehenergo", "Tatgazselkomplekt"), offer products of this plant. All foreign trade enterprises of Saratov, the south of Russia (Krasnodar, Rostov-on-Don, Stavropol) and Ufa offer mainly the production of "radon" - "signal". Their price depends on the discounts obtained at the factory, transportation and appetites of the management of firms. Competition can sometimes lead to significant savings opportunities for the consumer, as we see on the example of Krasnodar, where the price of Kubankägazservis is higher than the price of "centergazservis" by 40% (7,000 rubles).

The question arises: why, within the same city, there are similar variation of prices? The answer to it is not so obvious, as it seems. There is no doubt that the lack of consumer awareness plays a big role. But the main reason is different. Currently, neither in Krasnodar, nor in Russia there is no civilized PGO market - it is only created. Competition for a number of market segments is weak or not completely. It is competition that makes producers produce cheaper, more convenient to maintain, better equipment, which ultimately leads to a decrease in emergency situations. Normally working suppliers - units, mostly producers. At the same time, most existing manufacturers are focused on production, and not to work with consumers. A good supplier must be multigalender, that is, to maintain and offer equipment on the market of various manufacturers. It should be a trading company - manufacturers do not trade competitors products. Today, large trading companies, as a rule, offer consumers a higher quality service than manufacturers. We are pleased that, together with our parent company, the company "GAZ-SERVICE", Saratov (a trademark "Gazovik") - We make steps to build in Russia a civilized market for industrial gas equipment.

* Gas \u200b\u200bregulatory points (installations) are called a complex of technological equipment and devices designed to reduce the gas inlet pressure to a specified level and maintain it at the output permanent. Depending on the placement of the equipment, gas regulatory points are divided into several types: GRPS (gas regulatory clause) - equipment is placed in a metal cabinet; GRU (gas regulatory installation) - the equipment is mounted on a metal frame; PGB (Gas regulatory block) - the equipment is mounted in one or more container type buildings. For convenience, all gas management items (settings) described above are referred to in this article. However, it should be borne in mind that, as a rule, almost all manufacturers are produced both a grip and GRU, and the PGB with the same technological equipment.

Description

The demand for gas heating boilers in Russia in 2007-2011 grew and amounted to 852 thousand pcs in 2011. The decline in demand by 32% was recorded only in 2009, which is due to the crisis situation in the country's economy. During the economic crisis, most large construction projects were suspended, part of which was the installation of gas boiler equipment at facilities. Nevertheless, the gas heating equipment market in Russia experts recognize quite promising. According to BUSINESSTAT, in 2012-2016, the demand for gas heating boilers will grow and in 2016 will reach 1099 thousand pieces.

In the structure of demand for gas heating boilers, sales prevail in the domestic market. The volume of internal sales of gas heating boilers from 2007 to 2011 increased and amounted to 827 thousand pieces in 2011. A decrease in sales of gas heating boilers was observed only during the period of the economic crisis in 2009 by 33% in 2008

The volume of export supplies of gas heating boilers from Russia is significantly inferior to the volume of imported deliveries to the country. However, in 2007-2011, exports of Ros and in 2011 reached 24.1 thousand pieces. The main direction of the export of boilers from Russia has become Kazakhstan.

The supply of gas heating boilers in 2007-2011 also increased in 2011 amounted to 1034 pcs. In a five-year period, the proposal dynamics repeated the dynamics of demand: the reduction of the proposal was noted in 2009 by 27%.

The production of gas heating boilers in Russia in 2007-2011 decreased and in 2011 amounted to 209 thousand pieces. The negative dynamics demonstrated until 2010 inclusive. Production growth was recorded only in 2011 by 25%.

The maximum contribution to the structure of the supply of gas heating boilers is imported. The volume of imports into the country from 2007 to 2011 increased by 45%. The main importers became Italy and Germany.

"Analysis of the gas heating boilery market in Russia in 2007-2011, forecast for 2012-2016" Includes the most important data necessary to understand the current market opportuncture and estimates of its development prospects:

- Economic situation in Russia

- Manufacturers manufacturing and prices

- Sales and prices of gas heating boilers

- Balance of demand, supply, warehouse reserves of gas heating boilers

- Consumer number and consumption of gas heating boilers

- Export and import gas heating boilers

- Ratings of enterprises in terms of production and sales revenue

The review contains separately data on leading gas heating boilers:Lemax, Zhukovsky Machine-Building Plant, Star - Arrow, Condord, Gas Standard, Gastep Salervice, Kirov Plant, Novosergievsky Mechanical Plant, Saratov Plant of Energy Engineering, Borisoglebsky Boiler-Mechanical Plant, Mounting and Repair Management, Izhevsky Boiler Plant, Belogorier, Gas Kambar Equipment, Ziosab-Don, Tyumen-Diesel, Heat Heer, Siblenzodis, Union, Heat Silvervis, etc.

Businesstat prepares overview of the global gas heating boiler market, as well as the reviews of the CIS, EU and individual countries of the world. In the review of the Russian market, information is detailed by regions of the country.

When preparing the review used official statistics:

- Federal State Statistics Service of the Russian Federation

- Ministry of Economic Development of the Russian Federation

- Federal Customs Service of the Russian Federation

- Federal Tax Service of the Russian Federation

- Customs Union EurAsome

- world Trade organisation

- Association of Trading Companies and Commodity Producers of Electromete and Computer Technology RATEK

Along with official statistics, the review shows the results of own research BUSINESSTAT:

- Consumer survey large household appliances

- Retail audit of large household appliances

- Survey of market experts of large household appliances

Expand

ContentState of the Russian economy

- Basic parameters of the Russian economy

- Results of Russia's accession to the Customs Union

- Results of Russia's accession to the WTO

- Perspectives of the Russian economy

Classification of gas heating boilers

Demand and supply of gas heating boilers

- Sentence

- Demand

- Balance of supply and demand

Operation of gas heating boilers

- Lifetime

Assortment of gas heating boilers

Sales of gas heating boilers

- Natural sales

- Value sales

- Retail price

- Retail price and inflation ratio

- Natural, value sales and retail price ratio

- Number of buyers and purchase volume

Gas heating boilers

- Price manufacturers

Producers of heating boilers

- Production indicators of enterprises

- Financial indicators of enterprises

Export and import gas heating boilers

- Export and Import Balance

- Natural volume export

- Value exports

- Export price

- Natural import volume

- Cost import

- Price import

Economic indicators of the industry

- Financial result of the industry

- Economic efficiency of the industry

- Investment industry.

- Labor resources industry

Economic profiles of major manufacturers

- Registration data of the organization

- Management management

- Subsidiaries

- Major shareholders organization

- Production volume by product

- Balance of the enterprise in form n1

- Report on the profits and loss of the enterprise in form number 2

- The main financial performance of the enterprise

Expand

TablesThe report contains 80 tables

Table 1. Volume of nominal and real GDP, Russia, 2007-2016 (trillion rubles)

Table 2. The volume of real GDP and the index of the real physical volume of GDP, Russia, 2007-2016 (trillion rubles,%)

Table 3. Investments in fixed assets at the expense of all sources of financing, Russia, 2007-2016 (trillion rubles,%)

Table 4. Export and import and balance of trade balance, Russia, 2007-2016 (billion dollars)

Table 5. Average annual dollar exchange rate to ruble, Russia, 2007-2016 (rub for dollars,%)

Table 6. Consumer price index (inflation) and producer price index, Russia, 2007-2016 (% of the previous year)

Table 7. The population is based on migrants, Russia, 2007-2016 (million people)

Table 8. Really disposable incomes of the population, Russia, 2007-2016 (% of the previous year)

Table 9. Suggestion of gas heating boilers, Russia, 2007-2011 (thousands of thousands,%)

Table 10. Forecast of gas heating boilers, Russia, 2012-2016 (thousands of thousands,%)

Table 11. Production, import and warehouse reserves of gas heating boilers, Russia, 2007-2011 (thousand thousand)

Table 12. Forecast of production, import and warehouse reserves of gas heating boilers, Russia, 2011-GG (thousand pieces)

Table 13. Demand for gas heating boilers, Russia, 2007-2011 (thousands)

Table 14. Forecast for gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 15. Sales and exports of gas heating boilers, Russia, 2007-2011 (thousands of thousands)

Table 16. Sales forecast and exports of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 17. Balance of supply and supply of gas heating boilers, taking into account warehouse balances at the end of the year, Russia, 2007-2011 (thousands of thousands)

Table 18. Forecast of supply and supply of gas heating boilers, taking into account warehouse residues at the end of the year, Russia, 2012-2016 (thousands of thousands)

Table 19. Number of gas heating boilers in operation, Russia, 2007-2011 (thousands of thousands;%)

Table 20. Forecast of the number of gas heating boilers in operation, Russia, 2012-2016 (thousands of thousands;%)

Table 21. The number of gas heating boilers in the operation on the household consumer, Russia, 2007-2011 (PC;%)

Table 22. Forecast of the number of gas heating boilers in operation on the household-consumer, Russia, 2012-2016 (pcs;%)

Table 23. Middle Lifetime of gas heating boilers, Russia, 2007-2011 (thousands of thousands)

Table 24. Forecast of the average operation of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 25. Number of names of gas heating boilers on leading brand, Russia, 2011 (PC)

Table 26. Amplitude of prices for gas heating boilers on Markami, Russia, 2011 (rub)

Table 27. The structure of the range of gas heating boilers - the main characteristics

Table 28. Sales of gas heating boilers, Russia, 2007-2011 (thousands)

Table 29. Forecast of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 30. Sales of gas heating boilers, Russia, 2007-2011 (million rubles,%)

Table 31. Forecast of revenue from sales of gas heating boilers, Russia, 2012-2016 (million rubles,%)

Table 32. Retail price of gas heating boilers, Russia, 2007-2011 (thousand rubles per pcs)

Table 33. Retail price forecast of gas heating boilers, Russia, 2012-2016 (thousand rubles per pcs)

Table 34. Retail price ratio of gas heating boilers and inflation, Russia, 2007-2011 (%)

Table 35. Forecast Retail price ratio of gas heating boilers and inflation, Russia, 2012-2016 (%)

Table 36. The ratio of natural, value volume of sales and retail prices of gas heating boilers, Russia, 2007-2011 (thousands of thousands of thousand rubles per pcs; million rubles)

Table 37. Forecast of the ratio of natural, value sales and retail price of gas heating boilers, Russia, 2012-2016 (thousands of thousands of thousand rubles per pcs; million rubles)

Table 38. Number of households of buyers of gas heating boilers, Russia, 2007-2011 (million d / x)

Table 39. Forecast of the number of households-buyers of gas heating boilers, Russia, 2012-2016 (million d / x)

Table 40. Share of households of buyers of gas heating boilers from all households of Russia, 2007-2011 (%)

Table 41. Forecast of the share of households-buyers of gas heating boilers from all households of Russia, 2012-2016 (%)

Table 42. Purchase level of gas heating boilers, Russia, 2007-2011 (pcs per year; rub per year)

Table 43. Forecast of the purchase level of gas heating boilers, Russia, 2012-2016 (pcs per year; rub per year)

Table 44. Production of gas heating boilers, Russia, 2007-2011 (thousands)

Table 45. Forecast of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 46. Production of gas heating boilers in the regions of the Russian Federation, Russia, 2007-2011 (thousands)

Table 47. Price of producers of gas heating boilers, Russia, 2007-2011 (thousand rubles per pcs)

Table 48. Forecast Prices of gas heating boilers, Russia, 2012-2016 (thousand rubles per pcs)

Table 53. Balance of export and import of gas heating boilers, Russia, 2007-2011 (thousands of thousands)

Table 54. Export balance forecast and gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 55. Export of gas heating boilers, Russia, 2007-2011 (thousands of thousands)

Table 56. Forecast of exports of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 57. Export of gas heating boilers by country of the world, Russia, 2007-2011 (thousands of thousands)

Table 58. Export of gas heating boilers, Russia, 2007-2011 (million dollars)

Table 59. Forecast of exports of gas heating boilers, Russia, 2012-2016 (million dollars)

Table 60. Export of gas heating boilers by country of the world, Russia, 2007-2011 (thousand dollars)

Table 61. Export price of gas heating boilers, Russia, 2007-2011 (dollars per pcs)

Table 62. Forecast Gas heating boilers export prices, Russia, 2012-2016 (dollars per pcs)

Table 63. Export price of gas heating boilers by country of the world, Russia, 2007-2011 (dollars per pcs)

Table 64. Import of gas heating boilers, Russia, 2007-2011 (thousands of thousands)

Table 65. Export of gas heating boilers, Russia, 2012-2016 (thousands of thousands)

Table 66. Import of gas heating boilers by country of the world, Russia, 2007-2011 (thousands of thousands)

Table 67. Cost import of gas heating boilers, Russia, 2007-2011 (million dollars)

Table 68. Forecast of value import of gas heating boilers, Russia, 2012-2016 (million dollars)

Table 69. Import of gas heating boilers by country of the world, Russia, 2007-2011 (thousand dollars)

Table 70. The price of importing gas heating boilers, Russia, 2007-2011 (dollars per pcs)

Table 71. Forecast price of import gas heating boilers, Russia, 2012-2016 (dollars per pcs)

Table 72. Price of import gas heating boilers, Russia, 2007-2011 (dollars per pcs)

Table 73. Revenue (net) from the sale of products, Russia, 2007-2011 (million rubles)

Table 74. Commercial and managerial expenses, Russia, 2007-2011 (million rubles)

Table 75. Product costs, Russia, 2007-2011 (billion rubles)

Table 76. Gross profit from sales of products, Russia, 2007-2011 (million rubles)

Table 77. Economic efficiency of the industry, Russia, 2007-2011 (%; times; day days)

Table 78. Investment in the industry, Russia, 2007-2011 (million rubles)

Table 79. Labor resources of the industry, Russia, 2007-2011 (thousand people; million rubles; thousand rubles per year)

Table 80. Middle salary in the industry, Russia, 2007-2011 (thousand rubles per year)

What happens on the Russian heating equipment market, and what awaits him in the near future? Of course, his condition, first of all, will be determined by the general economic situation in the country, which, however, is valid for any industry.

Gas heating boilers

According to the report "Analysis of the gas heating boiler market in Russia" prepared by BusinesStat, after 2014, when the natural volume of sales of household heating boilers in Russia reached its maximum - 1,027 thousand pieces, the demand for them began to decline: in the crisis of the next two Many enterprises and homeowners preferred to postpone the purchase. According to BUSINESSTAT forecasts, in 2017, the decline in sales will continue - up to 735 thousand pieces. This will be caused by the continuing fall in the income of the population, a decrease in the pace of housing and suspension of the implementation of a number of projects. In 2018, BusinesStat predicts the start of sales growth - up to 859 thousand pieces in 2020.

In the Russian market, gas boilers are leading, which is explained by the relatively low gas prices. According to Yuri Salazkina, General Director of BDR TRAMI RUS (Brands and De Dietrich), currently, sales leaders are standard household atmospheric boilers with a capacity of 24 kW with a closed combustion chamber. Unlike the countries of the EU, where condensing technologies are occupied by a significant market share, traditional heating techniques prevail in Russia. Although these technologies are presented in Russia, they are not so popular as in Europe, where energy efficiency increase is actively stimulated at the legislative level, including through the provision of subsidies.

Nevertheless, the constant increase in gas tariffs leads to the fact that the Russian market moves towards more energy efficient heating equipment. So, the company launches on the Russian market a new brand of condensation boilers - ELCO. The first consumers will see the THISION L ECO model, which the manufacturer positions as the "top of engineering thought", and during 2017 there will also be a line of improved floor boilers R600 and R3400 (left). These boilers intended for use in autonomous heating systems and direct heating of DHW are distinguished by low weight and compactness, low noise and emissions.

Also among the latest new products in the gas boiler segment - a new line of Ariston Alteas X with an intelligent remote control system Ariston Net. With it, you can control the boiler and control its condition over the Internet from any smartphone or PC, which allows you to significantly reduce heating costs. Imagine: Leave on vacation, you lower the temperature in the apartment to a minimum, and a few hours before your return right from the airport, you install a comfortable mode. The application allows independently set the temperature of various zones and automatically maintain it taking into account weather conditions.

Alternative to Gas.

In places where there is no main natural gas, electric and solid fuel boilers are relevant. One of the interesting innovations in this segment is a unique Gilles boiler, working on manufacturing waste from the company. It is designed for industrial sites and farms, where there are waste production, which can with benefit from disposal - wooden sawdust, sunflower seed husks, grains, wet seeds, etc. On the Russian market of such equipment has not yet been.

Perhaps other progressive technologies will come to the Russian market. Hartmut Vessenberg, General Director of Lennox, one of the world's leading manufacturers of heating equipment, in an interview with the expert magazine, spoke that his company proposes to consider the possibility of applying in Russia, in particular, in Siberia air heating systems. These technologies that have already gained widespread in the world, but so far almost not used in our country have a number of advantages over traditional water (boiler) heating: safety associated with the lack of a liquid coolant, high speed of premises and efficiency - the cost of its operation on 20-30% lower, and the efficiency is almost twice as high as traditional systems. Well, and, importantly, these systems are available at a price.

Radiators heating

The most notable trend of last year is a significant decrease in imports into Russia aluminum and bimetallic heating radiators. This is due to the three main factors:

Weakening ruble;

Strengthening control by the federal customs service, which practically stopped the import of low-quality heating devices (mainly from the PRC);

Active Association of manufacturers of radiators of heating "APRO", which is struggling for the introduction of mandatory certification of heating devices.

These three factors had a positive impact on the development of the Russian production of heating radiators. According to the Deputy Chairman of the Committee of the Federation Council on the Economic Policy of Sergey Shatirov, according to preliminary data, the share of Russian products in the market increased from 22-24% in 2015 to 34% in 2016. Obviously, the tendency to increase the share of Russian manufacturers in the heating radiators sector will continue in 2017 - there are all prerequisites for this. Chairman of the Board of Directors of the TPC "RUSKLIMAT" Mikhail Tymoshenko made the following forecast for 2017: "Judging by the declared new projects, the potential of Russian producers of aluminum and bimetallic radiators - 20-25 million sections in production volumes and 45-50% in domestic consumption "

Investment projects of Western European companies will also contribute to this. Thus, the Italian representative of the International Association of Manufacturers of Aluminum Radiators AIRAL reported on the start of construction in Russia new industries, despite European sanctions against Russia.

During the parliamentary hearings of the Committee on Economic Policy dedicated to the imports of the heating systems, which took place in the Federation Council in early December 2016, a proposal was launched on providing domestic manufacturers of heating devices of a 15-percent price advantage with participation in state and municipal procurement. This will certainly also contribute to an increase in the share of domestic manufacturers in the Russian heating equipment market.