The capitalization of the company is determined. Capitalization ratio

Capitalization- an economic term used in the following meanings:

1. An increase in the volume of the company's own funds as a result of the transformation of dividends, surplus value, all or part of the profit into additional production objects (equipment, means and objects of labor, personnel) or into additional capital. In this case, the essence of capitalization is the transformation of future income into capital. Capitalized funds replenish the capitalist accumulation fund.

2. Analysis of the value of the company or its property, where the parameters for the assessment are:

The volume of working and fixed capital;

Market value of securities issued by the company (shares and bonds);

The size of the profit received each year.

In the banking sector, capitalization consists in issuing shares, increasing the existing capital by attaching the rate of return to interest and other operations to increase the capital base.

Depending on the activities carried out, a distinction is made between capitalization of income (appraisal of the value of firms) and market (stock) capitalization of a company (appraisal of the value of securities).

Good day, my dear visitors and readers. Today we will talk about the level of the company's capitalization and what can negatively affect it. Yes, this topic is quite far from trading and cryptocurrencies, but in terms of economics and general development, I think this topic will be useful.

In addition, the assessment of the company's capitalization is a very important factor that must be taken into account. If you are a potential investor and want to invest in the shares of a particular company, then assessing the level of capitalization is an important issue that you should consider. In general, I will try to explain in simple language what can negatively affect the level of capitalization itself.

RISK OF CHANGE IN PRICES FOR GOODS

There is always a risk that sharp fluctuations in the prices of a particular product may negatively affect the profile company and the level of its capitalization. For example, if a company sells goods, then a sharp increase in these goods will be beneficial and, conversely, if the price of goods decreases, then the company will be unprofitable and its level of capitalization may fall.

On the other hand, if a specialized company is engaged in the purchase of goods, then a decrease in their cost will play into the hands of both it and the level of capitalization, but an increase in this value will be a negative factor for the company and the level of capitalization.

Since this is about price, it will be appropriate to look at how to approach the issue when it is important.

But, in fact, I will say that these risks can affect even those enterprises that have nothing to do with goods. For example, a sharp rise in the cost of goods can force the population of a country to save, which, of course, will affect the service sector in general.

NEGATIVE MEDIA COVERAGE

This is a direct risk that the company's business, and its capitalization level, accordingly, may suffer from negative media coverage. The flow of news today is limitless, because no company can insure against this.

For example, the news about the accident at the Fukushima nuclear power plant in 2011 caused a wild resonance in the market, and the shares of many Japanese companies simply plummeted in price, with it the level of capitalization. The market is people, and people tend to panic, therefore, this or that news can cause a wild reaction from the market. It is clear that more global news can cause even bigger trouble, ranging from stock market crashes to a deep crisis in the country.

It is worth understanding that the market is a reflection of the opinions of people. People can react ambiguously to various force majeure circumstances, because emotions come into play. And where there are emotions, there is no longer a place for cold calculation, accordingly, it is impossible to predict the reaction, which is why, after the publication of unexpected news, the market can flounder terribly!

RISK OF RATING CHANGE

As a rule, there is a so-called credit rating, within which a certain economic assessment is assigned to an enterprise, which may change over time. There is something like this for those companies whose shares are traded on the stock exchange. In this case, there is a special rating of analysts, where the shares are assigned certain ratings.

It is clear that such expert assessments can become a serious psychological trigger. For example, imagine that a company's stock had a high valuation, but a year later, when new valuations were issued, it turned out to be significantly worse than the previous year. It is clear that this can negatively affect the level of capitalization, which will be a consequence of the fall in the level of share prices, as investors will simply start to shake them off.

WATCH VIDEO PREVIEW OF THE ARTICLE

Again, a subtle psychological thread is at work here. It is once again shown that behind all these prices are people, their expectations, hopes, fears and intentions. These all sorts of ratings are often tracked by investors, and on the basis of this information, they then think about how to proceed with their investments in the future.

RISK OF BECOMING ANACHRONISM

This is the risk that the company's business could become a kind of dinosaur, only in economic terms. It should be understood that there are not so many really successful companies, and even fewer of those companies that have been operating for a very long time, that is, they live to see their 100th anniversary.

The market is very dynamic, it is changing, therefore, if a company does not adapt to it and change its business concept at the right times, then it may well become that very dinosaur. The market is, first of all, tough competition, and with the further improvement of modern technologies, this competition becomes even more fierce. In this case, over time, a competitor may always appear who will provide a similar product, but of a higher quality and at a reduced price. It is clear that then the company will systematically fall into stagnation, and there it is not far from bankruptcy.

DETECTION OF PARTS BY AUTHORITIES

In this case, we are talking about the fact that the conditional auditor can find some piquant details from the company that can lead to the collapse of the system itself. It can be anything: theft by management, fraud, bogus reporting, and so on.

If such information emerges, then it can cause irreparable damage to the company's image. After such a serious blow, it will be very difficult to withstand. In fact, such cases are not isolated, for example, the ENRON company.

LEGISLATIVE RISK

Here we are talking about the relationship between the direction of business and current legislation. In this case, the government can impose restrictions specifically on the company or on the industry as a whole. It is clear that all this will negatively affect the investments of people who have invested their money in a company or industry.

In theory, the government acts as a kind of buffer between business and the population of the country. The government will intervene whenever business clearly puts pressure on society or fails to self-regulate. But in reality, governments often reinsure themselves by initiating, at times, completely stupid laws that unreasonably squeeze business.

INFLATION AND INTEREST RATES

For example, if interest rates rise, then a business that needs funding may run into problems. Roughly speaking, the costs of this company will increase, and it will be much more difficult to stay afloat.

For example, if the increase in interest rates is at the level of inflation, then the company may face problems, as the purchasing power of money falls. In general, inflation and interest rate hikes can occur both separately and simultaneously, which can have a negative effect on the company.

RISK OF THE MODEL

There is always the risk that the general model or concept that underlies the business may become wrong. Companies that use it suffer from the wrong model. In this case, a certain domino effect can often be triggered, when large companies will pull other smaller companies to the bottom.

For example, the mortgage crisis that took place in the period 2008-2009 clearly showed that an initially incorrect model can have serious negative effects even on the economies of large countries.

CONCLUSIONS

In general, if we talk about risks, then I say again that risks are part of the business, and there is no way to supplant them. There is no company, line of business or even economy that is not exposed to risks. In addition, I would like to remind you that the market is a living ecosystem that is capable of reacting very aggressively to any changes in the market.

The bottom line is that markets are not always rational. Any force majeure news has a very strong impact on the market. As I have said many times, where there are emotions, there is no rationality, and accordingly, it makes no sense to predict something.

In general, business and trading overlap very strongly. I would say that trading is a kind of business line, therefore, in order to be successful here, you must first of all think like a real businessman. Business acumen, they either exist or not, it's very simple!

Well, this is the kind of material, and I hope it will be useful to you. I will say goodbye to you, I wish you good luck and see you soon!

Market capitalization- a value indicator that allows you to analyze the general attitude of investors towards a particular company. Although it is listed side by side on the official websites of companies next to parameters such as EBITDA or P / E, it is difficult to call it a multiple due to bias. Rather, it is a basic metric for calculating more accurate multiples, such as net debt. Read on to learn more about how to calculate the market cap of a company and the disadvantages of the indicator.

Market capitalization: what it is and how the indicator can be useful for an investor

Market capitalization reflects the total value of the outstanding shares held by investors and owners of a company. The indicator is used to superficially assess the value of a company and analyze its dynamics over a certain period of time.

There is a total market capitalization and stock market valuation of the common shares in circulation. Many sources interpret market capitalization as multiplying the market price of one share by the number of shares outstanding, but this is an even less accurate indicator for evaluating a company. Correct would be a correction for the so-called capital dilution, which may include:

- options to buy shares;

- preference shares;

- convertible bonds.

The financial statements will tell you about the presence of such securities in the company's capital, but it will be difficult to find information about them on the official website without experience. Therefore, I recommend to be guided by the optimal formula:

Market capitalization = number of common shares * current market price + number of preferred shares * current market price

All information for the calculation is freely available.

Benefits of market capitalization for investors

- to assess the dynamics of capitalization growth at different time intervals, on the basis of which a decision on investment can be made;

- to analyze how stock prices and capitalization react to certain fundamental factors. How sensitive is the company's value to force majeure or vice versa to positive market signals. The greater the sensitivity, the greater the risk, but the more you can earn from volatility.

In my opinion, it is not advisable to compare the capitalization of companies in the same industry, as well as the cost of a single share. For example, the dynamics of Gazprom shares, despite its capitalization of almost 3 trillion rubles, is not the most attractive for investors, and the value of VTB Bank shares is calculated in kopecks at all and therefore cannot be compared, for example, with Sberbank shares.

Derivative multiples based on capitalization: PE Ratio, PS Ratio, Price Book Ratio.

Disadvantages of evaluating a company based on market capitalization

- the presence of a speculative component in the share price. For example, traditionally, before the payment of dividends, there is an increase in quotations of securities, after payments - a rollback. The financial condition of the company remains unchanged, capitalization changes;

- ignoring other influential economic factors in the indicator. Investors who know how to analyze financial statements compare the market value of shares with the debt burden and liquid assets of the company. But there are investors who invest money, guided by the good dynamics of quotations and someone's advice. It is they who unreasonably overstate the market value of securities;

- limited ability to evaluate. Only publicly traded companies for which basic information is available can be estimated by market capitalization.

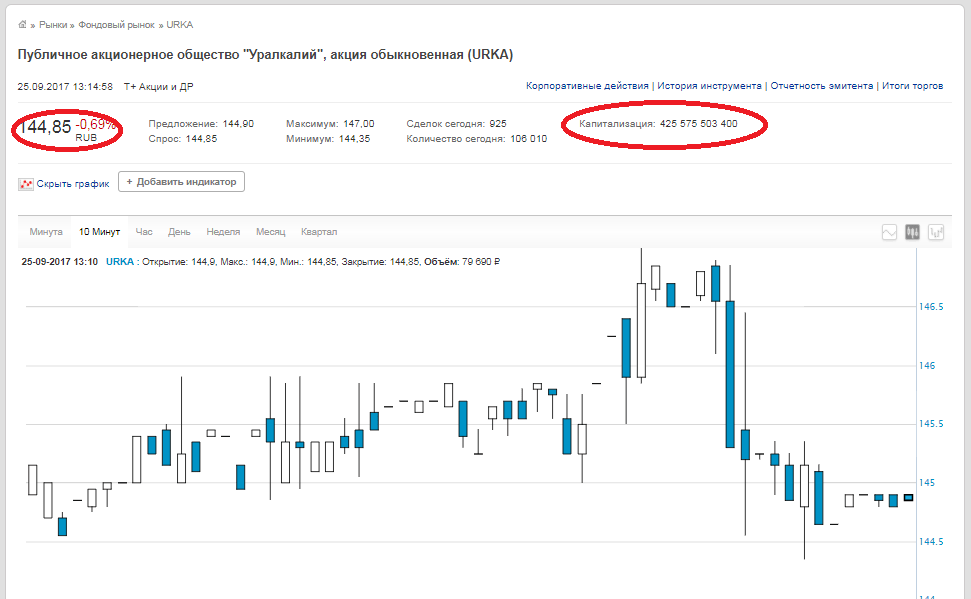

A practical example of calculating the market capitalization of a company

All data on the number of shares and their current value is available both on the websites of the companies themselves and analytical resources, and on the exchange itself. Let's take PJSC Uralkali as an example. The number of ordinary shares - 2,936,015,891,

closing price - 144.85 rubles (data as of September 25, 2017). We multiply these figures with each other and we get a market value of 425.575 billion rubles. The same figure is on the exchange website.

Please note that on the stock exchange website, the line “Capitalization” does not indicate the capitalization of the company, but the capitalization of the share, that is, if the company has ordinary shares and preferred shares, then these two numbers must be added to obtain the company's market capitalization.

Output... Calculating market capitalization versus calculating multiples of EBITDA, P / E or net debt is very simple and straightforward. But it serves only as a generalized indicator and has large errors. I would not recommend relying solely on the dynamics of the share price at the time of making a decision to invest. You need to analyze all indicators and multipliers in a complex.

Market capitalization is used to calculate many other useful and useful multiples, which I will write about a little later.

M.V. Dedkova JSCB "Settlement United Union European Bank"

Scientific publication FGOU VPO RGUTiS, journal "Vestnik MGUS" Issue "Economics", No. 1 for 2007

Capitalization is one of the few economic phenomena in which an extremely high interest is shown in practice and which, until recently, has been extremely insufficiently studied in the domestic economic literature. Independent research in the field of capitalization has appeared only in recent years. These include A.S. Permyakov's dissertations. on the topic "Investment support and capitalization management of oil and gas companies", Ovsyannikova A.N. on the topic "Capitalization of industrial enterprises in Russia as a factor in increasing their economic stability", Yezhova Yu.V. on the topic "The method of capitalization of the amortization fund of a machine-building enterprise", Kazintseva V.V. on the topic "Market capitalization of Russian industrial corporations as a factor in increasing the economic efficiency of production", Hovsepyan D.E. on the topic "Capitalization Management of Industrial Corporations", Pivenya V.V. on the topic "Modeling the influence of economic factors on the market capitalization of industrial corporations", Galtseva E.V. on the topic "Capitalization as a factor in strengthening the financial stability of enterprises in the service sector", Varoko A.Sh. on the topic "Capitalization management of investment resources of the reproductive potential of the agro-industrial complex of the region."

Thus, the list of independent research in the field of capitalization is so small that it can be cited almost in full. In most of the above studies, capitalization is considered from the perspective of increasing the company's equity capital. At the same time, the emphasis is mainly on joint stock companies, the shares of which are in free float. In this case, capitalization is assessed based on the market value of the shares. This is the most common approach to capitalization in the domestic market, borrowed from foreign practice. Due to this, it has a very limited scope of application in the domestic economic environment, where the share capital has not yet become widespread. Consequently, with this approach to capitalization, most of the Russian companies drop out of the research object.

Only in the study of E.V. Galtseva. an attempt has been made to show various forms of capitalization manifestation in the Russian market. Depending on the mechanism for increasing capitalization, the author identifies three of its forms:

- real capitalization;

- marketing or subjective capitalization;

- market or fictitious capitalization.

All of the above forms of capitalization are reflected in the balance sheet of companies in the form of building up their own sources of financing (section 3 of the balance sheet), however, they have different sources of origin and different methods of initiation.

Real capitalization

An efficiently operating enterprise almost always has a positive financial result of economic activity. Profit, or rather its reinvested part, accumulates in section 3 of the balance sheet, largely determines the value of the enterprise and leads to an increase in equity capital. High capitalization indicates the ability of an economic entity to generate income, efficiently use resources, expand the business, which, in turn, is a condition for future profitability.

Meanwhile, an increase in the 3 section of the balance sheet, other things being equal, means an increase in the liability and, therefore, by virtue of the basic rule of balance sheet management, causes an increase in the asset of an economic entity. Depending on the type of activity, the strategy of the enterprise and the current problems that have developed, the increase affects either non-current or current assets, or both at the same time. If, as a result of financial and economic activities, the enterprise reinvests profits, directing it to replenish non-current assets (primarily means of labor) and current assets (in terms of items of labor or stocks), real capitalization occurs, expressed in an increase in the real value of property. In most cases, enterprises with a strong strategy invest their capital gains in long-term assets, i.e. in section 1 - non-current assets.

In this case, capitalization is a natural result of financial and economic activities, is economically objective and is initiated by funding sources, i.e. balance liabilities. Real capitalization leads to the strengthening of the financial stability of the company, an increase in its credit rating, an increase in marketing attractiveness and an increase in its market value.

Marketing or subjective capitalization

In practice, the accumulation process at the on-farm level is often the result of an active marketing policy and advertising campaign, which "wind up" the market value of the enterprise, tearing it away from the real value. In this case, the increase in the balance sheet currency, other things being equal, occurs initially from the side of assets, as a rule, the intangible component of the balance sheet, for example, due to the following operations:

- reflection in the balance sheet of the valuation of business reputation (goodwill);

- increasing the market value of a trade mark, brand;

- reflection in accounting and, accordingly, in the know-how balance;

- acquisition of rights to the results of intellectual activity.

An increase in the property of an enterprise in this case, other things being equal, can be reflected in the balance sheet in different ways:

- balance in liabilities with the growth of additional capital;

- relate to financial results, increasing retained earnings;

- increase the authorized capital with appropriate registration in accordance with the established procedure.

Additional capital, retained earnings and authorized capital, in turn, increase the “equity capital” aggregate. In this case, capitalization is initiated by intra-firm management on the part of assets, primarily intangible assets. Valuation in this case is often contractual, therefore, subjective. The increase in property due to contractual valuations, even at the cost of re-registration of the authorized capital, is to a large extent a subjective operation. Transactions of this kind make it possible to form a “representative” balance sheet of the company, however, given that intangible assets are high-risk assets, such capitalization can disappear with the slightest change in the political situation or market conditions. An increase in equity capital due to the expansion of the authorized capital gives operations of this kind a certain stability and legal form, however, it represents an extensive path of enterprise development and does not indicate the effectiveness of using its potential. This type of capitalization is called subjective or marketing capitalization, since its nature is subjective, and this form of capitalization is used, as a rule, for marketing purposes.

Subjective (marketing) capitalization has recently become very popular among PR agencies, which proceed from the fact that business reputation plays a key role in shaping the value of a company. This approach to capitalization led to the emergence of the Reputation Capitalization project initiated by the Publicity PR Agency. In an expert survey conducted by this PR agency, 1,072 respondents from among top managers, heads and employees of marketing, advertising and PR departments, financial analysts and other experts of large companies took part, more than 60% of respondents answered that business reputation is real. value-creating asset.

In the development of subjective (marketing) capitalization in Russia, previously property taxation served as a deterrent. However, the "containment" was insignificant, given the low property tax rate. Currently, only fixed assets, reflected in the balance sheet at their residual value, are taxed. This means that almost any enterprise can increase capitalization with small funds and form a “representative” balance sheet, which, in turn, will cause the activation of the subjective (marketing) form of capitalization in the Russian market.

Market or fictitious capitalization.

At developed stages of a market economy, where joint-stock ownership, free circulation of shares and the determination of the market value of an enterprise through stock quotes are widespread, the understanding of capitalization as interpreted by Richard Koch is more acceptable. R. Koch believes that capitalization is “the market value of a company whose shares are quoted on the stock exchange”, which is the product of the market price of a share and the total number of shares of the company. The increase in the market value of shares and the joint-stock company as a whole is reflected in this case in the asset of the balance sheet in the form of revaluation of financial investments "and is balanced in liabilities by additional capital.

This form of manifestation of capitalization has obvious similarities with subjective (marketing) capitalization. However, capitalization in this case is initiated not by intra-firm management, but by external exchange structures that carry out quotations of shares. The results of exchange trading, as you know, are formed under the influence of a combination of objective and subjective factors, but the effect of subjective factors is minimized by public recognition.

In academic publications, capital represented in income-generating securities is referred to as fictitious or stock capital. Since this form of capitalization is formed as a result of stock transactions, it is called fictitious capitalization. Stock market analysts prefer to call this form of capitalization manifestation market capitalization.

In Russia, fictitious or market capitalization has recently been developing, which is due to the activation of the stock market. However, it is typical only for large Russian business formed on a joint-stock form of ownership. For the majority of domestic enterprises, this tool for building up equity capital, hence this form of capitalization, is not yet available.

Along with the listed forms of manifestation of capitalization, one can single out such concepts as “capitalization of property” and “capitalization of expenses”.

Capitalization of property is manifested in an absolute and relative increase in capital property - non-current assets, which are the most attractive collateral in any financial transactions and the most significant component of the company's real property. The most promising and manageable part of non-current assets are intangible assets. These include marketing strategy, customer base, market monitoring methodology and marketing research results, know-how, high reputation and qualified personnel, long-term relationships with customers, and much more. The valuation of intangible assets and their reflection in accounting is an acceptable tool for capitalizing property.

Capitalization of expenditures means the conversion of part of current expenditures into expenditures of a capital nature. A classic example of capitalizing on spending would be advertising spending, which is a recurring cost, but the result is a brand that can be valued in the billions of dollars. It is generally recognized by the business community that a brand is an intangible asset and one of the most important competitive advantages of a company. However, its cost estimates and trends in their change over time do not fit into the traditional rules of reflection in accounting for intangible assets. Thus, intangible assets are depreciable, i.e. the transfer of their cost to the cost of the newly created product / service is made in parts by calculating depreciation. Upon the expiration of the useful life of the intangible asset, its value is nullified. A brand can not only not lose its value over time, but also increase it. Being an intangible asset according to all the characteristics listed above, the brand needs a special procedure for assessment and revaluation. Only in this case will capitalization of expenses become possible, as a result of which it will be possible to increase the value of non-current assets by reflecting the brand in their composition.

It should also be noted that up to now, the capitalization toolkit in various types of activities has not been sufficiently studied. The most studied in this regard is industrial capitalization. Meanwhile, in the conditions of a service society, capitalization in various sectors of the service sector needs additional research.

The study of the practical experience of capitalization, its comprehensive analysis and theoretical generalizations are important for all market participants: for enterprises that form their own image in the market, for their partners, for shareholders.

Literature

1. Galtseva E.V. Capitalization as a factor in strengthening the financial stability of enterprises in the service sector: Dis. Cand. economy, sciences. M., 2005.137 p.

2. Koch R. Management and finance from A to Z. SPb .: Peter, 1999. 496 s.

3. Soviet encyclopedic dictionary. 3rd ed. Moscow: Soviet Encyclopedia, 1984.100 p.

4. Economic encyclopedia. Political Economy. Moscow: Soviet Encyclopedia, 1975.T. 4.672 p.

Capitalization - the value of a company in the market

The capitalization of a company is the aggregate current value of its shares traded on the market (the market, exchange value of one share is also called its capitalization).

K comp = N com * R com + K priv * P priv,

where P com, P priv - respectively the market value of common and preferred shares.

The market price of ordinary shares is RUB 18.15.

K comp = 746 018 770 000 * 18.15 + 263 300 742 000 * 18.15 = 18 319 149.14 million rubles.

Capitalization Ratios - the ratio of borrowed funds and total capitalization. Capitalization ratios reflect the degree to which a company uses its equity capital efficiently.

share of bonds

K region = (par value of bonds / (par value of bonds + par value of com. Shares + par. Value of priv. Shares + profit for distribution)) * 100% = (10 156 672 / (10 156 672 + 37 300 938.45 + 6 582 518.55 + 3 423 101)) * 100% = 17.6%

share of ordinary shares

K com = (par value of ordinary shares / (par. Value of bonds + par. Value of com. Shares + par. Value of priv. Shares + profit to be distributed)) * 100% = (37,300,938.45 / ( 10 156 672 + 37 300 938.45 + 6 582 518.55 + 3 423 101)) * 100% = 64.9%

specific preferred shares

K pr.obl = (par value of preferred shares / (par value of bond + par value of com. Shares + par value of privileged shares + profit for distribution)) * 100% = (6 582 518, 55 / (10 156 672 + 37 300 938. 45 + 6 582 518, 55 + 3 423 101)) * 100% = 11,4%

Conclusion

So, a security is not money or a tangible commodity. Its value lies in the rights that it, as a specific monetary document, gives to its owner. Changes in the relationship of various property rights regarding the ownership and lending, disposal and management of securities form the basis of the stock market.

Based on the calculations of the cost of securities of OJSC KAMAZ, the following conclusions can be drawn:

· As of December 31, 2007, the authorized capital of KAMAZ OJSC is made up of the par value of outstanding ordinary and preferred shares of KAMAZ OJSC in the amount of 746,018,770,000 pieces for the amount of 37,300,938.45 million rubles. and 263,300,742,000 pieces for the amount of 6,582,518.55 million rubles. respectively;

· The size of the authorized capital of KAMAZ OJSC as of December 31, 2007. amounts to 43 883 457 million rubles;

· Net working capital of KAMAZ OJSC is 12,998,265 million rubles . Net working capital is necessary to maintain the financial stability of the enterprise, since the excess of working capital over short-term liabilities means that the company not only can pay off its short-term liabilities, but also has financial resources to expand its activities in the future.

· The liquid capital is 18,764,725 million rubles. Net liquid assets are equal to 6 798 039 million rubles. and shows that liabilities in the balance sheet liability are covered by assets.

· The inventory turnover ratio is 3.66, that is, the inventory goes through 3.66 cycles of full renewal or full sale within a certain period of time;

Net tangible assets attributable to 1 bond issued in circulation amount to RUB 1,893,350 .

· Net tangible assets attributable to 1 preferred and ordinary shares issued in circulation are, respectively, 170 rubles. and 10 rubles. in accordance with the data of accounting and reporting;

· The coefficient of profitability of OJSC KAMAZ from production activities is 6.28%;

· The profitability ratio is 5.27%, that is, each ruble of products sold brought 5.27% of profit;

· The current yield on bonds, declared by the issuer, is 25% of the par value of the bonds, in value terms this amount is 25,289,168 million rubles .;

· Calculating the return on equity capital, we found that for every ruble of capital there are 10 kopecks of net profit. 1 placed share accounted for 1.1 rubles. authorized capital;

· The ratio of "financial leverage" of OJSC KAMAZ is 1.47. Borrowed funds exceed own funds, but not significantly. Financial leverage allows you to optimize the ratio between equity and borrowed funds in order to maximize the return on equity. The quantitative expression of financial leverage shows the increase in net profitability of equity, due to the use of borrowed funds;

· The share of securities in the equity capital of KAMAZ OJSC is:

Corporate bonds - 17.6%

Ordinary shares - 64.9%

Preferred shares - 11.4%

· Capitalization of OJSC KAMAZ is 18,319,149. 14 million rubles. To date, the market value of ordinary shares is 18.15 rubles. The level of capitalization of KAMAZ OJSC has grown significantly in recent years.

According to the AK&M agency, for the reporting year OJSC KAMAZ ranks 18th in the rating of shares in terms of growth in the market capitalization of enterprises at the end of December 2007. Such a rapid growth in the company's capitalization was caused by several factors:

· Fundamental underestimation of the company's shares, which existed before 2007, as a result of the consequences of “market distrust” in the company's ability to overcome the consequences of the financial crisis of the 90s caused by the default of the Russian economy;

· Significant improvement in financial and operational performance of the company in 2006 and 2007, favorable forecasts for further development;

· The interest of investors in companies whose growth is directly related to the development of infrastructure in the Russian Federation;

· Increasing the transparency of the company: since 2007, the company regularly publishes financial statements in accordance with IFRS (international financial reporting standards), which are audited by PricewaterhouseCoopers;

· Increased transparency of the company: KAMAZ began to hold meetings with investors and bank analysts on a regular basis, participate in conferences and organized a department for work with investors;

· Repurchase of own shares in the amount of 10% and their further redemption and reduction of the authorized capital carried out in 2007;

On the whole, over the period from 2000 to 2007, the capitalization of KAMAZ OJSC increased 24.4 times. As a result, KAMAZ OJSC ranks second in terms of capitalization among mechanical engineering enterprises at the end of 2007.

It is planned to sell a stake in KAMAZ OJSC to a strategic investor Daimler AG in 2009 at a price higher than the current market value, which currently does not reflect the company's fundamental value, and may become a driver of growth in KAMAZ shares in the short term. In addition, thanks to the development of cooperation with a large successful foreign company operating in the market for the production of trucks, the fundamental value of KAMAZ OJSC in the long term should increase due to the implementation of new projects to expand the model range and improve the consumer properties of the products.

In addition, the sale of the package to a strategic investor will allow KAMAZ to gain access to the technologies of its partner, which will expand the model range and improve the consumer properties of the products. This will have a positive impact on the fundamental value of the company in the long term. In turn, Daimler AG will gain access to the rapidly growing Russian market, about one third of which is occupied by OJSC KAMAZ.

According to experts, the fair value of 1 ordinary share of KAMAZ OJSC is $ 3.44, which implies a 107% upside potential and corresponds to a Buy recommendation.

Bibliography

1. Galavanov VA Securities market: Textbook. - 2nd ed., Rev. and add. - M .: Finance and statistics, 2006. - 448 p .: ill.