Collection and processing of information for making management decisions. Models and methods of decision making

Read also

Preparation and decision-making in the management process is a set of procedures combined into separate stages. With all the variety of such procedures, the stages of development and decision-making are quite typical. Thanks to this, it is possible to build a general scheme for developing scientifically based management decisions, based on the principles of a systems approach and methods of systems analysis. To achieve success, it is extremely important not only to make a reasonable, expedient, justified, effective decision, but also to take measures to ensure its practical implementation.

Preparation and decision-making in the management process is a set of procedures combined into separate stages. With all the variety of such procedures, the stages of development and decision-making are quite typical. Thanks to this, it is possible to build a general scheme for developing scientifically based management decisions, based on the principles of a systems approach and methods of systems analysis.

General procedural and technological scheme for making management decisions:

- Identification, analysis, diagnosis of the problem.

- Formation of goals and objectives for solving a problem, taking into account limitations.

- Analysis of ways to solve problems and management decisions that are adequate to them.

- Modeling scenario options, assessing the results and consequences of implementing different options.

- Choosing the preferred option, justifying the choice.

- Making a management decision.

- Bringing the decision to execution.

- Management of solution implementation.

The most typical problems, the occurrence of which leads to the need to make management decisions:

- the state of the managed object and the processes occurring in it has come into conflict with the goals of its activities recorded in laws, plans, programs, regulations, charters;

- the functioning of the facility and its performance indicators contradict norms, standards, and requirements, which threatens the loss of stability;

- the needs for the product of the facility’s activities have changed, the market situation has transformed, and therefore it is necessary to make changes to the functioning of the facility;

- an unforeseen emergency situation arose, conditions in the external environment changed dramatically;

- new potential opportunities have emerged to significantly improve the condition and operation of the facility;

- decisions of higher authorities have been adopted obliging them to make fundamental changes in the activities of the management object and to carry out the measures prescribed by these authorities.

Management experts rightly note that identifying a problem in a timely and correct manner means half solving it. Therefore, identifying problems, understanding their essence and correctly interpreting them is an integral part of the decision-making process.

Taking into account the fact that management decisions are closely related to penetration into the essence of problems, the presence of which initiates the solution process itself, the need is obvious not only to identify the presence of a problem, but also to diagnose it. Diagnostics is designed to establish the nature of the problem, its content, degree of urgency, relationship with other problems, types and scale of dangers arising from the problem. Diagnostics is based on the study, analysis, and research of the symptoms of the problem, that is, observable signs indicating its presence.

The danger of confusing the problem and its symptoms should be avoided. The problem is most often characterized by a number of signs and symptoms that give reason to assume its presence, while only individual symptoms allow one to gain confidence in the existence of the problem and in its true essence. And we must strive to eliminate not the symptoms of the problematic disease, but to cure the disease itself, which is the solution to the problem.

A significant role in identifying and analyzing problems that need to be solved is played by the information used, obtained inside or outside the analyzed system. Along with the requirements for the quantity and quality of the information received, its composition and representativeness are no less important. It is well known that excess information is just as harmful as its insufficiency. It is even more important to have the necessary information directly related to the matter, to the problem being studied; such information in control theory is called relevant. To obtain relevant information, it is necessary to resort to filtering processes of all received data in order to select only those that are directly related to the occurrence and essence of the problem being analyzed.

The main sources of information used in the process of identifying problems, preparing and making decisions are internal and external reporting and statistical data, scientific literature, reviews, legislative and regulatory acts, regulations, instructions, foreign analogues, expert assessments, and attitudes of decision makers.

At the second stage of the decision-making process, it is necessary to formulate and formulate the goals and objectives of the solution being prepared. From a clearly defined goal, tasks are drawn more clearly. At the same time, the formulation of goals and objectives is inevitably affected by the psychology and interests of those involved in the analysis, preparation, development of a decision and, especially, its adoption.

The set of restrictions that must be observed when setting goals and objectives, making choices and making decisions forms the area of acceptable decisions. Within this area, a search should be made for options and alternatives considered at subsequent stages of the decision-making process.

Let us note that failure to comply with restrictions is one of the main reasons for making obviously ineffective, unrealistic, or even simply erroneous management decisions. The root cause of such imperfection is that at the stages of preparation and search for rational solutions, restrictive conditions are not analyzed, not fully taken into account, or simply not taken into account. A correctly organized, rationally organized process of developing and making management decisions should include the formulation and analysis of restrictions, the formation of a zone of existence of acceptable decisions.

Among the most creative operations and procedures in the process of developing and making management decisions are the search and formation of a set of alternatives (methods, options) for solving the problem under consideration and the corresponding control actions. The wider the range of alternatives for solving a problem, the greater the chances of finding the most rational, and ultimately the optimal, solution. At the same time, it is practically impossible and impractical to find and compare all possible alternatives. The search and analysis of many options require significant expenditures of money, labor, and time, which in itself can reduce the effectiveness of the best solutions found. As always in such situations, there is some “golden mean”. In the process of searching for alternatives, macroeconomic solutions are limited to 3-4 options, and microeconomic ones - 4-5.

In conditions of limited time, there is a tendency to reduce the finding and comparison of options to finding not the best, but an acceptable solution. In this case, it is considered acceptable to consider a solution option that allows you to significantly weaken or basically eliminate the problem within the available time at an acceptable cost of resources. Analysts within the framework of this approach act on the principle “the best is the enemy of the good” and stop increasing the number of options being studied as soon as among the selected ones there are already options acceptable to the decision maker.

It is also desirable that the alternatives selected for comparison differ significantly from each other in the ways of solving the problem, and thereby in the depth and time of the solution, and the resources spent. If this condition is met, the likelihood of subsequent selection of the most favorable solution option increases. Comparable parameters of differing alternatives include the timing and results of implementing a given solution option, the resources expended, and the expected consequences of the analyzed methods of action.

The key stage in making a management decision is the operation of selecting a preferred alternative from the list of those considered and analyzed. Such a choice is preceded by a comparison and comparison of options based on a range of parameters established during modeling and forecasting, including, first of all, indicators of the degree of solution to the problem, solution time, resource costs, expected consequences of the decision, and the degree of risk of non-fulfillment of the decision.

When choosing the preferred option, justifying their choice, and making the final decision, all participants in this process are forced to consider and take into account a number of outcome indicators: the cost of resources and time, risk, and the consequences of the decision. According to some indicators, some compared options are preferable, and according to other parameters, other options are preferable. Most often, a deeper solution to a problem requires more resources and longer time. Therefore, the choice of the optimal solution can be discussed with a significant degree of convention, since there is no single criterion for the optimality of solutions, with rare exceptions.

In the conditions of a typical multicriteria choice, preference is given to an acceptable option, which seems to be the best from certain positions to decision makers. Quite often, the contribution of the chosen option for solving a problem to the solution of other problems, the expected reaction to the choice of option on the part of interested parties and the interests of the decision maker are taken into account.

The validity of a decision largely depends on the depth of its elaboration, the consistency of the above stages and procedures for developing decisions. To do this, it is necessary to provide for the iterative nature of the entire process with a possible return from subsequent operations to previous ones.

To achieve success, it is extremely important not only to make a reasonable, expedient, justified, effective decision, but also to take measures to ensure its practical implementation. It is necessary to bring the decision to the performers and inform the entire circle of participants in the execution about it. It is also required to organize management of the implementation of the decision made at all stages of its implementation in accordance with a specially developed schedule.

Boris Raizberg

1. TECHNOLOGY AND PROCEDURES FOR DEVELOPMENT AND MAKING MANAGEMENT DECISIONS

1.6. Decision making based on information systems and controlling

1.6.1. The role of information in decision making

in strategic management

In modern business conditions, the role of effective management based on reliable information increases many times over. Management errors based on insufficient or misinterpreted data can lead to the collapse of even large companies. The most interesting technologies and rules of management and planning are provided by strategic management, which deals with the development and implementation of the company's strategy. There are many definitions of this concept, but in a general sense, strategy is a long-term plan for managing a company, aimed at strengthening its position, satisfying customers and achieving its goals. Executives (managers) develop strategy to determine what direction the company will take and make informed decisions when choosing a course of action. The choice of a specific strategy by managers means that from all the possible development paths and methods of action open to the company, it is decided to choose one strategic direction in which the company will develop. Without a strategy, a manager has no thought-out plan of action, no guide to the business world, and no unified program for achieving the desired results.

The company management plan covers all main functions and divisions: supply, production, finance, marketing, personnel, R&D. Everyone has a specific role to play in this strategy. Making strategic choices means tying together business decisions and competitive actions across the company into a single node. This unity of actions and approaches reflects the current strategy of the company. New actions and approaches being discussed using all available information will show possible ways to change and transform the current strategy.

A good strategic vision prepares a company for the future, sets long-term directions for development, and defines the company's intention to take specific business positions. In other words, strategic management views an enterprise as a complex system, which in turn operates in even larger systems: target market, industry, national market, etc.

Today, strategic management is a very quickly and dynamically developing scientific and practical activity, which is not surprising, because its development is determined by the needs of the modern market. Companies around the world are using new methods and tools of strategic management to reconsider the way they do business, focus on business, ensure competitiveness and achieve better results in their field.

One of the most powerful tools in the hands of a manager is information. Effective management is impossible without collecting information and processing it using various methods. Methods for obtaining information are varied and are not the subject of consideration in this work. Of much greater interest are the methods of its processing and targeted distribution to recipients. Methods for processing and analyzing economic information constitute the essence of econometrics. The second is the question of building an integrated information system, aimed at solving problems facing the enterprise and being a reflection of ongoing business processes.

The role of strategic management and planning is great. Good management today certainly requires managers to have strategic thinking and the ability to formulate, develop a strategy and, most importantly, successfully implement it. Managers have to think globally (that is, without abstracting from external and internal factors) about the situation in which the company finds itself and the impact that changing conditions have on it.

A modern manager must have extraordinary analytical skills that would allow him to adequately evaluate current and specially collected information relating to the entire range of external and internal factors. This is necessary in order to set realistic goals, adjust them (goals) in time and, as a result, adjust the means of achieving them.

In other words, strategic management is the foundation of an overall approach to managing the entire company. One CEO put it well: “Basically, our competitors know the same fundamental concepts, methods, and approaches that we do, and they are as well equipped to follow them as we are. Often the difference between their success and ours is the relative care and discipline with which they and we develop and execute our strategies for the future.”

The advantages of a strategic approach to management (as opposed to free improvisation, intuition or inactivity) based on the intensive use of information systems are:

ensuring that the organization's ideas are focused on the key strategy question “what are we going to do and what are we achieving?”

the need for managers to more clearly respond to emerging changes, new opportunities and threatening trends;

the opportunity for managers to evaluate alternative options for capital investment and staff expansion, i.e. wisely transfer resources to strategically sound and highly effective projects;

the ability to combine decisions of managers at all levels of management related to strategy.

Summarizing all of the above, we can draw the following conclusion: strategic management is a systematic approach to enterprise management, which is the most effective.

1.6.2. The essence of controlling

Today there is no unambiguous definition of the concept of “controlling,” but almost no one denies that this is a new management concept generated by the practice of modern management. Controlling (from the English control - management, regulation, management, control) is far from being limited to control. This new concept of system management of an organization is based on the desire to ensure the successful functioning of the organizational system (enterprises, trading companies, banks, etc.) in the long term by:

adapting strategic goals to changing environmental conditions;

coordination of operational plans with the strategic plan for the development of the organizational system;

coordination and integration of operational plans for various business processes;

creating a system for providing managers with information for various levels of management at optimal intervals;

creating a system for monitoring the implementation of plans, adjusting their content and implementation deadlines;

adaptation of the organizational structure of enterprise management in order to increase its flexibility and ability to quickly respond to changing requirements of the external environment.

One of the main reasons for the emergence and implementation of the controlling concept was the need for systemic integration of various aspects of business process management in the organizational system. Controlling provides a methodological and instrumental basis to support the basic functions of management: planning, control, accounting and analysis, as well as assessing the situation to make management decisions.

It should be emphasized that controlling is not a system that automatically ensures the success of an enterprise by freeing managers from management functions. This is only a management tool, but a very effective one.

The key components of the controlling concept are:

orientation towards the effective operation of the organization in a relatively long-term perspective - a philosophy of profitability, the formation of an organizational structure focused on achieving strategic and tactical goals;

creation of an information system adequate to the tasks of target management;

dividing controlling tasks into cycles, which ensures iterative planning, monitoring execution and making corrective decisions.

Controlling functions and tasks. Controlling as a management system concept served as a response to changes in the external conditions of the functioning of organizations (enterprises). There has been an evolution of the organization's management functions. Planning for individual aspects was transformed into comprehensive program-target planning, sales and marketing management - into marketing, accounting and production accounting - into a control and regulation system. In general, the observed evolution of organizational management functions with their integration into the controlling system reflects the main trend of an integrated approach to management.

Controlling is focused primarily on supporting processes decision making. It must ensure the adaptation of the traditional accounting system at the enterprise to the information needs of decision-makers, i.e. Controlling functions include the creation, processing, verification and presentation of system management information. Controlling also supports and coordinates the processes of planning, information provision, control and adaptation.

The goals of controlling, as an area of activity, directly follow from the goals of the organization and can be expressed in economic terms, for example, in achieving a certain level of profit, profitability or productivity of the organization at a given level of liquidity.

Controlling functions are determined by the goals set for the organization and include those types of management activities that ensure the achievement of these goals. This includes: accounting, support for the planning process, monitoring the implementation of plans, assessing ongoing processes, identifying deviations, their causes and developing recommendations for management to eliminate the reasons that caused these deviations.

In the field of accounting, controlling tasks include creating a system for collecting and processing information essential for making management decisions at different levels of management. This is necessary for the development and further maintenance of a system for maintaining internal records of information about the progress of technological processes. Important are the selection or development of accounting methods, as well as criteria for assessing the activities of the enterprise as a whole and its individual divisions.

Support for the planning process consists of performing the following controlling tasks:

formation and development of a comprehensive planning system;

development of planning methods;

determination of information necessary for planning, sources of information and ways to obtain it.

The controlling system informationally supports the development of basic plans for the enterprise (sales, liquidity, investments, etc.), coordinates individual plans in terms of time and content, checks the plans for completeness and feasibility, and allows the creation of a single operational (annual) plan for the enterprise. The controlling system determines how and when to plan, and also evaluates the feasibility of implementing planned actions.

The controlling service does not determine what to plan, but advises how and when to plan and assesses the feasibility of implementing planned activities. Responsibility for the implementation of plans remains within the competence of line managers.

When providing analytical information to the organization's management, the tasks of controlling include:

standardization of information channels and media;

choice of information processing methods.

The controlling system must ensure the collection, processing and provision to management of information essential for making management decisions.

In each individual case, the functions of the controlling service depend on many circumstances, but if we generalize the existing practice of enterprises, we can obtain an ideal list of the main functions and tasks of controlling, presented below.

We divide the main functions and tasks of controlling into the following groups: accounting, planning, control and regulation, information and analytical support, special functions. Let us describe the composition of each of these groups.

collection and processing of information;

development and maintenance of an internal accounting system;

unification of methods and criteria for assessing the activities of an organization and its divisions.

Planning:

information support in the development of basic plans (sales, production, investment, procurement);

formation and improvement of the entire “architecture” of the planning system;

establishing information and time requirements for individual steps in the planning process;

coordination of the information exchange process;

coordination and aggregation of individual plans by time and content;

checking proposed plans for completeness and feasibility;

drawing up a master plan for the enterprise.

Control and regulation:

determination of quantities controlled in time and content;

comparison of planned and actual values to measure and evaluate the degree of goal achievement;

determination of permissible limits of deviations of values;

analysis of deviations, interpretation of the reasons for deviations of the plan from the fact and development of proposals to reduce deviations.

Information and analytical support:

development of information system architecture;

standardization of information media and channels;

provision of digital materials that would allow for control and management of the organization;

collection and systematization of the most significant data for decision-making;

development of tools for planning, control and decision-making;

consultations on the selection of corrective measures and solutions;

ensuring cost-effective operation of the information system.

Special Features:

collection and analysis of data on the external environment: the state of financial markets, industry conditions, government economic programs, etc.;

comparison with competitors;

justification for the feasibility of merging with other companies or opening (closing) branches;

Conducting cost estimates for special orders;

calculations of the effectiveness of investment projects, etc.

Based on the above list of functions and tasks of controlling, one can quite clearly imagine the scope of its application. The scope of controlling functions implemented in organizations depends mainly on the following factors:

economic condition of the organization;

understanding by management and/or owners of the organization of the importance and usefulness of implementing controlling functions;

size of the organization (number of employees, volume of production);

level of production diversification, range of products;

the current level of competition;

qualifications of management personnel;

qualifications of the controlling service employees.

In large organizations, it is advisable to create a specialized controlling service. Small organizations, as a rule, do not have such a service in their structure. In small enterprises, the main controlling functions are performed either by the head of the company or his deputy. At the same time, many tasks are integrated and simplified. For example, the tasks of developing plans, coordinating them and checking for feasibility can be considered as a single task if it is performed by the head of the enterprise himself. Small enterprises very rarely solve the problem of buying other companies or selling branches. In a medium-sized enterprise with single-industry production, the scope of functions and tasks of accounting, planning and reporting will naturally be smaller compared to a multi-industry enterprise.

In the context of the deteriorating economic situation at the enterprise, which is manifested in a decrease in the level of liquidity and profitability, controlling services are expected to provide more services for coordinating plans, analyzing the reasons for deviations of plans from reality, as well as recommendations for ensuring survival in the near future.

1.6.3. Business reengineering

To successfully implement changes planned in a company, it is necessary to clearly understand that each business unit requires continuous design. Continuous engineering involves approaching business as a process. A process is a sequence of economic acts (tasks, work, relationships) determined in advance by business goals. It is sometimes said that a business process is a set of steps that a company takes from one state to another, or from “input” to “output”. The inputs and outputs here are not parts of the company or its divisions, but events. The overall management of business and business processes is called “business engineering,” which involves the ongoing design of processes—determining inputs, outputs, and sequences of steps—within a business unit.

Nowadays, the concept of business reengineering is becoming popular in the design of business processes. The founder of reengineering theory, M. Hammer, defined this concept as follows: “a fundamental rethinking and radical change in decisions about business processes in order to achieve dramatic improvements in critical performance indicators such as costs, quality, service and speed.”

Reengineering has the following properties:

he abandons outdated rules and regulations and begins the business process as if from a “clean slate”, this allows him to overcome the negative impact of dogmas;

he neglects the existing systems, structures and procedures of the company and radically changes, reinvents the methods of economic activity - if it is impossible to remake your business environment, then you can remake your business;

it leads to significant changes in performance indicators.

Reengineering is used in three main situations:

in conditions where the company is in a state of deep crisis;

in conditions where the current position of the company is satisfactory, but the forecasts for its activities are quite unfavorable;

in situations where aggressive, prosperous organizations seek to increase their lead over competitors and create unique competitive advantages.

Main stages of reengineering:

formation of the desired image of the company (the basic elements of the construction are the company’s strategy, main guidelines, ways to achieve them);

creating a model of the company’s existing business (to create the model, the results of an analysis of the organizational environment and controlling data are used; processes that need restructuring are identified);

development of a new business model - direct reengineering (selected processes are redesigned, new personnel functions are formed, new information systems are created, a new model is tested);

introduction of a new business model.

1.6.4. Enterprise Management Information Systems (EMIS)

Let's start with the definitions necessary to understand further discussions.

Information is information about the surrounding world (objects, phenomena, events, processes, etc.), which reduces the existing degree of uncertainty, incomplete knowledge, alienated from their creator and become messages (expressed in a certain language in the form of signs, including recorded on a tangible medium) that can be reproduced by transmission by people orally, in writing or by other means.

The information allows organizations to:

exercise control over the current state of the organization, its divisions and processes in them;

determine the strategic, tactical and operational goals and objectives of the organization;

make informed and timely decisions;

coordinate the actions of departments in achieving goals.

Information need is a conscious understanding of the difference between individual knowledge about a subject and the knowledge accumulated by society.

Data is information reduced to the level of an object of certain transformations.

Document – an information message in paper, audio, electronic or other form, drawn up according to certain rules, certified in the prescribed manner.

Document flow is a system for creating, interpreting, transmitting, receiving, archiving documents, as well as monitoring their execution and protecting them from unauthorized access.

Economic information is a set of information about socio-economic processes that serve to manage these processes and groups of people in the production and non-production sphere.

Information resources – the entire available amount of information in the information system.

Information technology is a system of methods and methods for collecting, transmitting, accumulating, processing, storing, presenting and using information.

Automation is the replacement of human activity with the work of machines and mechanisms.

Information system (IS) is an information circuit together with means of collecting, transmitting, processing and storing information, as well as personnel performing these actions with information.

The mission of information systems is the production of information necessary for the organization to ensure effective management of all its resources, the creation of an information and technological environment for the management of the organization.

Typically, management systems have three levels: strategic, tactical and operational. Each of these management levels has its own tasks, when solving which there is a need for relevant data; this data can be obtained by querying the information system. These requests are directed to the corresponding information in the information system. Information technologies make it possible to process requests and, using available information, generate a response to these requests. Thus, at each level of management, information appears that serves as the basis for making appropriate decisions.

As a result of the application of information technologies to information resources, some new information or information in a new form is created. These products of the information system are called information products and services.

An information product or service is a specific service when some information content in the form of a set of data, generated by the manufacturer for distribution in tangible and intangible form, is provided for use by the consumer.

Currently, there is an opinion about an information system as a system implemented using computer technology. This is wrong. Like information technologies, information systems can function both with and without the use of technical means. This is a matter of economic feasibility.

Advantages of manual (paper) systems:

ease of implementation of existing solutions;

they are easy to understand and require minimal training to master;

no technical skills required;

they are typically flexible and adaptable to suit business processes.

Advantages of automated systems:

in an automated IS, it becomes possible to holistically and comprehensively present everything that happens to the organization, since all economic factors and resources are displayed in a single information form in the form of data.

Corporate IP is usually considered as a certain set of private solutions and components of their implementation, including:

unified information storage database;

a set of application systems created by different companies and using different technologies.

The company's information system (in particular, ISMS) must:

allow the accumulation of certain experience and knowledge, generalize them in the form of formalized procedures and solution algorithms;

constantly improve and develop;

quickly adapt to changes in the external environment and new needs of the organization;

meet the urgent requirements of a person, his experience, knowledge, psychology.

Creating an enterprise management information system is a rather time-consuming and resource-intensive process, in which four main stages can be distinguished.

1. Project sketch. A detailed description of the goals and objectives of the project, available resources, any restrictions, etc.

2. Project evaluation. It determines what the system will do, how it will operate, what hardware and software will be used, and how it will be maintained. A list of requirements for the system is being prepared, and the needs of regular users are being studied.

3. Construction and testing. Personnel must ensure that the system is easy to use before it becomes the mainstay of operations.

Project management and risk assessment. The project is not complete until the project manager can demonstrate that the system works reliably.

The life cycle of an IS is the period of creation and use of an IS, covering its various states, starting from the moment the need for this IS arises and ending with the moment of its complete decommissioning.

The IS life cycle is divided into the following stages:

pre-project survey;

design;

IP development;

putting the IS into operation;

exploitation of IP;

completion of operation of the IS.

So, an enterprise management information system (EMIS) is an operating environment that is capable of providing managers and specialists with up-to-date and reliable information about all business processes of the enterprise necessary for planning operations, their execution, registration and analysis. In other words, a modern PMIS is a system that contains a description of the full market cycle - from business planning to analysis of the results of the enterprise. In reality, they often start with partial computerization of information processes, for example, within the framework of accounting or warehouse management.

1.6.5.PMIS tasks

Managing enterprises in modern conditions requires increasing efficiency. Therefore, the use of enterprise management information systems (EMIS) is one of the most important levers for business development.

Particular tasks solved by the PMIS are largely determined by the area of activity, structure and other features of specific enterprises. As examples, we can refer to the experience of creating an information management system for an enterprise - a telecom operator and the experience of implementing SAP R/3 systems by partners at a number of enterprises in the CIS and non-CIS countries. At the same time, an approximate list of management tasks that an ISMS should solve at various levels of enterprise management and for its various services can now be considered generally accepted among specialists. It is shown in Table 1. When solving these problems, various methods of decision theory are widely used, including econometric and optimization.

Table 1.

Main tasks of the ISMS

|

Management levels and services |

Problems to be solved |

|

|

1 |

Enterprise management |

providing reliable information about the current financial condition of the company and preparing a forecast for the future; Ensuring control over the work of enterprise services; Ensuring clear coordination of work and resources; Providing operational information about negative trends, their causes and possible measures to correct the situation; formation of a complete picture of the cost of the final product (service) by cost components |

|

Financial and accounting services |

Full control over the movement of funds; Implementation of the accounting policies required by management; Prompt determination of receivables and payables; Monitoring the implementation of contracts, estimates and plans; Control over financial discipline; Tracking the movement of inventory flows; Prompt receipt of a complete set of financial reporting documents |

|

|

3 |

Manufacturing control |

control over the implementation of production orders; Monitoring the state of production facilities; Control over technological discipline; Maintaining documents to support production orders (fence maps, route maps); prompt determination of the actual cost of production orders |

|

Marketing Services |

Control over the promotion of new products to the market; Analysis of the sales market with the aim of expanding it; Maintaining sales statistics; Information support for price and discount policies; Using a database of standard letters for mailing; control over the fulfillment of deliveries to the customer on time while optimizing transportation costs |

|

|

5 |

Sales and supply services |

Maintaining databases of goods, products, services; Planning delivery times and transportation costs; Optimization of transport routes and transportation methods; Computerized contract management |

|

6 |

Warehouse accounting services |

Management of a multi-echelon warehouse structure; Operational search for goods (products) in warehouses; Optimal placement in warehouses taking into account storage conditions; revenue management taking into account quality control; inventory |

1.6.6. Place of PMIS in the controlling system

Management information systems are computer support for controlling, which in turn is the main supplier of information for enterprise management. The purpose of information support for controlling is to provide management with information about the current state of affairs of the enterprise and predict the consequences of changes in the internal or external environment. The main tasks of controlling are presented in Table 2.

Table 2.

Main tasks of controlling

|

Main tasks to be solved |

||

|

Controlling in a management system |

The goal of strategic controlling is to ensure the continued successful functioning of the organization. The main task of operational controlling is to provide methodological, informational and instrumental support to enterprise managers |

|

|

Financial controlling |

Maintaining profitability and ensuring liquidity of the enterprise |

|

|

Controlling in production |

Information support for production and management processes |

|

|

Marketing Controlling |

Information support for effective management to meet customer needs |

|

|

Controlling resource provision |

Information support for the process of acquiring production resources, analysis of purchased resources, calculation of the efficiency of the supply department |

|

|

Controlling in the field of logistics |

Current control over the efficiency of storage and transportation of material resources |

Let's compare (in accordance with Table 3) the main tasks that are solved by PMIS and controlling (see Table 1 and Table 2).

Table 3.

Comparison of PMIS and controlling tasks

|

MIS tasks solved for |

Controlling tasks solved |

|

Enterprise manuals |

Controlling in a management system |

|

Financial and accounting services |

Financial controlling |

|

Production management |

Controlling in production |

|

Marketing Services |

Marketing Controlling |

|

Sales and supply services |

Controlling resource provision |

|

Warehouse accounting services |

Controlling in the field of logistics |

From Table 3 it can be seen that the ISMS tasks solved for each level of management and service of the enterprise correspond to the tasks solved by controlling in one or another area of the enterprise’s activity (namely, controlling in the management system, financial controlling, etc.).

If we consider the structure of the ISMS, we can distinguish 5 main modules that are present in each information system. These are financial and economic management, accounting and personnel, warehouse, production, trade (sales).

An analysis of the 27 most famous PMIS presented on the Russian market (according to Internet data) was carried out in 2002 by E.A. Guskova. The results are presented in Table 4. We can conclude that only a few have a built-in controlling module (see Table 4).

Table 4.

Availability of a controlling module in Russian PMIS

|

The product's name |

Company |

Controlling module (+ - yes, 0 – no) |

|

|

Informcontact |

|||

|

Nikos-Soft |

|||

|

RS Balance ver. 2.7 |

|||

|

Altant-inform |

|||

|

Aleph Consulting&Soft |

|||

|

BOSS Corporation |

|||

|

Intellect service |

|||

|

Galaxy |

Galaxy |

||

|

Intalev:corporate finance |

|||

|

Laguna 2000 |

Accord soft |

||

|

LoKOFFICE |

|||

|

Client-server-technologies |

|||

|

Contact Manager module |

IBS TopS Lanit |

||

|

Monopoly |

Formosa-soft |

||

|

TB Corporation |

|||

|

TECTON, IntelGroup |

|||

|

TIS (trade information system) |

|||

|

Infosoft |

|||

|

Figaro-ERP |

Business Console |

||

1.6.7. Prospects for joint development of PMIS

and controlling

In order to look into the future, let's first try to go back to the past.

The development of methods of managing industrial enterprises at the beginning of the twentieth century is associated primarily with the names of G. Ford, F. Taylor, G. Gantt, A. Fayol and others. It was A. Fayol who divided the actions of the administration into a number of functions, which included forecasting and planning, creation of organizational structures, team management, coordination (of managers’ actions) and control. .

Inventory management model, leading to the "square root formula" for the optimal order size, proposed by F. Harris in 1915, but became famous after the publication of the well-known work of R. Wilson in 1934, and is therefore often called the Wilson model. The theory of inventory management received a powerful impetus in 1951 thanks to the works of K. Arrow (future Nobel laureate in economics), T. Harris, and J. Marshak. In 1952, the works of A. Dvoretsky, J. Kiefer, and J. Wolfowitz were published. In Russian, the theory of inventory management as a whole is discussed in the works of E. Bulinskaya 1964, J. Bukan, E. Keningsberg 1967, Y. Ryzhikov 1969, A. Orlov 1975 and 1979, etc.

It is necessary to note the work on the creation of an ISUP at the Kyiv Institute of Cybernetics of the Ukrainian SSR Academy of Sciences, created by B. Gnedenko in the 1950s (in 1961 this institute was headed by V.M. Glushkov). In the early 60s, work began on automation of inventory management. The end of the 60s is associated with the work of O. White, who, when developing automation systems for industrial enterprises, proposed considering production, supply and sales divisions as a whole. O. White's publications formulated planning algorithms, today known as MRP - material requirements planning- at the end of the 60s, and MRP II - Manufacturing Resource Planning- in the late 70s - early 80s. . Not all modern management concepts originated in the United States. So, the method of planning and management Just-in-time(“just in time”) appeared at the enterprises of the Japanese automobile concern in the 50s, and OPT methods - optimized technology production facilities were created in Israel in the 70s. Concept Computerized Integrated Manufacturing CIM arose in the early 80s and is associated with the integration of flexible production and management systems. Methods CALS - computer support for the supply and logistics process arose in the 80s in the US military department to improve the efficiency of management and planning in the process of ordering, developing, organizing production, supplying and operating military equipment. . System ERP – corporate resource planning proposed by the analyst firm Gartner Group not so long ago, in the early 90s, and has already confirmed its viability. . Systems CRM– customer relationship management became necessary in a highly competitive market, where the focus was not on the product, but on the customer. Much has been done in the USSR and in Russia, primarily at the Institute of Control Problems, the Central Institute of Economics and Mathematics, the All-Russian Scientific Research Institute for System Research and the Computing Center of the Russian Academy of Sciences.

Currently, the emphasis in enterprise resource planning (based on ERP systems) is shifting towards supporting and implementing supply chain management processes ( SCM systems), customer relationship management (CRM systems) and e-business (e-commerce systems).

Let's analyze the development trends of the Russian software market for automating the process of enterprise management. We can conclude that it is developing dynamically and the range of tasks that require automation is becoming more complex. At first, managers of Russian enterprises most often set simple tasks, in particular, the task of automating the accounting process. With the development of companies and the increasing complexity of business processes, the need arose not only for “post-mortem accounting”, but also for the management of material and technical supplies (logistics processes), work with debtors and creditors and many other tasks that the internal and external environment poses to the enterprise. . To solve these problems, corporate information management systems began to be used - solutions covering the activities of the entire enterprise.

Thus, as a result of “evolution,” the ISMS has transformed from computer accounting and an automated inventory management system into a comprehensive management system for the entire enterprise.

Currently, there are a large number of standard PMIS on the market - from local ones (costing up to 50 thousand US dollars) to large integrated ones (costing 500 thousand US dollars and more). Standard solutions of these PMIS are “tied” by supplier companies to the conditions of specific enterprises.

Note that currently the main part of the management system is not developed on the basis of standard solutions, but in a single copy for each individual enterprise. This is done by the relevant departments of enterprises in order to most fully take into account the characteristics of specific enterprises.

The classification of typical systems available on the Russian market is presented in Table 5. It was developed in .

Here is a description of the main types of PMIS.

· Local systems. As a rule, they are designed to automate activities in one or two areas. Often they can be a so-called “boxed” product. The cost of such solutions ranges from several thousand to several tens of thousands of US dollars.

· Financial and management systems. Such solutions have much greater functionality compared to local ones. However, their distinguishing feature is the absence of modules dedicated to production processes. And if in the first category only Russian systems are presented, then here the ratio of Russian and Western products is approximately equal. The implementation time of such systems can fluctuate around a year, and the cost can range from 50 thousand to 200 thousand US dollars. The systems designated in Table 5 as “transitional” are in the stage of transition to the class of medium integrated systems.

Table5.

ISUP classification

|

Local |

Financial and managerial |

Medium integrated |

Large integrated |

||

|

"Clean" |

"Transitional" |

||||

|

Western |

|||||

|

"Inotek" |

|||||

|

"Monopoly" |

|||||

|

And more than 100 systems |

|||||

|

Russian |

|||||

|

Galaxy |

|||||

|

Designers: “Alef”, “Softprom”, “Tekton”, “Etalon”, ABACUS, M2, etc. |

Specialized solutions: Hyperion, Business, Objects, PowerPlay |

||||

|

New players: Axapta, Brain, Mincom, Platinum ERA, Wonderware, etc. |

|||||

Note: systems are listed in alphabetical order throughout.

· Medium Integrated Systems. These systems are designed for production plant management and integrated production process planning. They are characterized by the presence of specialized functions. Such systems are most competitive on the domestic market in their area of specialization with large Western systems, while their cost is significantly (an order of magnitude or more) lower than large ones.

· Large integrated systems. Today, these are the most functionally developed and, accordingly, the most complex and expensive systems in which MRPII and ERP management standards are implemented. The implementation time of such systems, taking into account the automation of production management, can be several years, and the cost ranges from several hundred thousand to several tens of millions of dollars. It should be noted that these systems are intended primarily to improve the management efficiency of large enterprises and corporations. In this case, the requirements of accounting or personnel records fade into the background.

· Constructors is a commercial software tool, a set of software tools or a specialized programming environment for the relatively quick (compared to universal programming tools) creation of business applications based on the design invariant methodology and operating technology.

· Specialized solutions – are intended mainly for obtaining corporate consolidated reporting, planning, budgeting, data analysis using OLAP technology (on-line analytical processing - operational data analysis - multidimensional operational data analysis for decision support).

Econometric methods in PMIS. An analysis of the real needs of enterprises showed that to create a full-fledged system that would provide not only accounting functions, but also forecasting capabilities, scenario analysis, and support for management decision-making, the standard set of functions of ERP systems is not enough. Solving this class of problems requires the use of analytical systems and methods, primarily econometric, and the inclusion of these systems and methods in the PMIS.

Econometric methods are an important part of the scientific tools of the controller, and their computer implementation is an important part of the information support of controlling. In the practical application of econometric methods in the operation of the controller, it is necessary to use appropriate software systems. General statistical systems such as SPSS, Statgraphics, Statistica, ADDA, and more specialized Statcon, SPC, NADIS, REST (for interval data statistics), Matrixer and many others can also be useful.

PMIS in solving problems of controlling. To summarize, first of all, we note that PMIS plays an undeniably important role in solving controlling problems. But, knowing the importance and need for information support for controlling, it remains unclear why Russian developers are in no hurry to include the controlling module in the PMIS. After all, this is necessary so that the system provides not only computer support for controlling, but also provides managers and specialists with up-to-date and reliable information about all business processes of the enterprise, necessary for planning operations, their execution, registration and analysis. But it would also become a system that carries information about the full market cycle - from business planning to analysis of the results of the enterprise.

Having analyzed almost 30 Russian PMIS (see Table 4), it was not possible to answer this question.

Although the answer may lie in the cost of such a solution, as well as in the lack of awareness by the management of a number of enterprises of the relevance of the development and implementation of controlling. Therefore, the demand for such PMIS is still small. But positive trends are still emerging. So the next generation of the “M-2” system, the “M-3” software complex, developed by the “Client - Server - Technologies” company, is no longer positioned simply as an enterprise management system, but a product that forms a decision-making environment. In the M-3 complex there is a shift in emphasis: from a registration system to a structure that makes it possible to implement forecasting based on professional analysis. The basis for this is the implementation of the controlling mechanism, which involves the creation of a tool for making operational decisions in financial, production and other areas of enterprise activity.

In addition, the experience of Western companies shows that demand is gradually growing for large integrated systems, which are distinguished by the depth of management support for large multifunctional groups of enterprises (holdings or financial and industrial groups).

And if we talk about the development of the domestic PMIS industry and the widespread introduction of controlling into the work practices of Russian organizations and enterprises, we have to admit that for most Russian enterprises the stage of full-scale business informatization is just beginning.

Literature

1. Orlov A.I., Volkov D.L. Econometric methods in resource management and business information support for a telecom operator company. - Journal “Pridniprovsky scientific journal. Donbassky exit". Proceedings of the international scientific and technical conference "Problems and management practices in economic systems." Economics. No. 109 (176). Breast 1998

2. Vinogradov S.L. Controlling as a management technology. Practice notes // Controlling. – 2002. - No. 2.

3. Karminsky A.M., Dementyev A.V., Zhevaga A.A. Informatization of controlling in the financial and industrial group // Controlling. – 2002. - No. 2.

4. Karminsky A.M., Olenev N.I., Primak A.G., Falko S.G. Controlling in business. Methodological and practical foundations for building controlling in organizations. – M.: Finance and Statistics, 1998. – 256 p.

5. Management. Textbook/Ed. Zh.V. Prokofieva. – M.: Knowledge, 2000. – 288 p.

6. Orlov A.I. Sustainability in socio-economic models. – M.: Nauka, 1979. – 296 p.

7. White O. W. Management of production and inventories in the computer age. - M.: Progress. 1978. – 302 p.

8. Computer-integrated production and CALS technologies in mechanical engineering. - M.: Federal Information and Analytical Center for the Defense Industry. 1999. – 510 p.

9. Keller, Erik L. Enterprise Resource Planning. The changing application model. 1996. (http://www.gartnergroup.com).

10. Lyubavin A.A. Features of the modern methodology for implementing controlling in Russia // Controlling. – 2002. - No. 1.

11. Karpachev I. You’ll go left // Enterprise partner: corporate systems. - 2000. - No. 10.

12. Orlov A.I. Econometrics. – M.: Exam, 2002. – 576 p.

13. Orlov A.I. Econometric support for controlling // Controlling. 2002. - No. 1.

14. Internet representation of the company "Client - Server - Technologies" (http://www.m2system.ru).

15. Guskova E.A., Orlov A.I. Enterprise management information systems in solving controlling problems // Controlling. – 2003. - No. 1.

Control questions

1. What is the role of information in decision making?

2. What is the essence of controlling?

3. What are the main ideas of business reengineering?

4. Discuss the basic definitions in the field of enterprise management information systems.

5. What are the main objectives of the PMIS?

6. What is the place of the PMIS in the controlling system?

7. Give a classification of typical enterprise management information systems.

Topics of reports, abstracts, research works

1. The composition and movement of information arrays in an enterprise known to you.

2. History of the development of enterprise management information systems.

3. Circulation of paper and electronic documents.

4. Econometric methods in information systems.

5. The role of the Internet and corporate computer networks in enterprise management.

| Previous |

Despite the fact that the “process of information analysis” is rather a technical term, 90% of its content is related to human activity.

Understanding the needs at the heart of any information analysis task is closely related to understanding the company's business. Collecting data from suitable sources requires expertise in data collection, regardless of how much the final data collection process can be automated. In-depth knowledge of business processes and consulting skills are required to turn collected data into analytical insights and effectively apply them in practice.

The information analysis process is a cyclical flow of events that begins with an analysis of the needs in the area under consideration. This is followed by collecting information from secondary and/or primary sources, analyzing it and preparing a report for the decision makers who will use it, provide feedback and prepare suggestions.

At the international level, the process of information analysis is characterized as follows:

- First, decision-making steps are identified in key business processes and compared with standard end results of information analysis.

- The information analysis process begins with an international needs assessment, i.e. identifying future decision-making needs and testing them.

- The information collection stage is automated, which allows you to allocate time and resources for the primary analysis of information and, accordingly, increase the value of existing secondary information.

- A significant amount of time and resources are spent on information analysis, conclusions and interpretation.

- The resulting analytical information is brought to the attention of each decision-maker on an individual basis, with the process of its further use being monitored.

- Members of the group that analyzes information have a mindset of continuous improvement.

Introduction: Information Analysis Cycle

The term "information analysis process" refers to a continuous, iterative process that begins with identifying the information needs of decision makers and ends with providing the amount of information that meets those needs. In this regard, it is necessary to immediately distinguish between the volume of information and the process of analyzing information. Determining the scope of information is aimed at identifying the goals and needs for information resources for the entire information analysis program, while the process of information analysis begins with identifying the needs for one, even if insignificant, final result of such analysis.

The process of analyzing information should always be tied to existing processes in the company, that is, strategic planning, sales, marketing or product production management, within which this information will be used. In practice, the use of the information obtained at the output should either be directly related to decision-making situations, or such information should help to increase the level of awareness of the organization in those areas of operational activities that are related to various business processes.

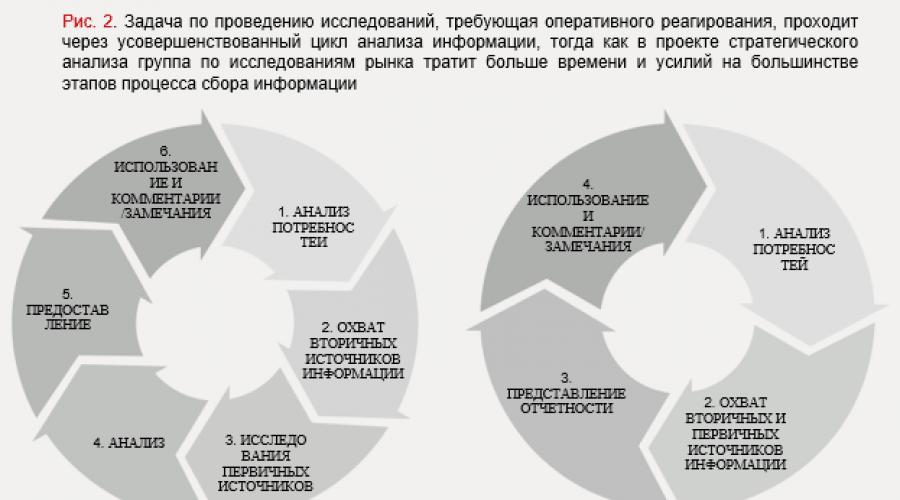

In Fig. Figure 1 shows the stages of the cyclical process of information analysis (see below for more details). In turn, the right side of the diagram shows the specific results of the information analysis process, when decisions are made on the basis of general market research, and the results of the information analysis process directly related to various business processes and projects.

Click on the image to enlarge it

The information analysis cycle consists of six stages. Their detailed description is given below.

1. Needs analysis

A thorough needs assessment allows you to determine the goals and scope of the information analysis task. Even if those solving such a problem will collect information for their own use, it makes sense to clearly identify the key directions in solving this problem in order to concentrate resources in the most appropriate areas. However, in the vast majority of cases, those who conduct research are not the end users of its results. Therefore, they must have a full understanding of what the end results will be used for, to avoid collecting and analyzing data that may ultimately not be relevant to users. For the needs analysis stage, various templates and questionnaires have been developed that set a high quality bar at the initial stage of solving the problem.

However, the most important thing is that the organization's information analysis needs must be fully understood and transformed from external to internal in order for the information analysis program to be of any value. Templates and questionnaires alone cannot achieve this goal. They can naturally be useful, but there have been times when an excellent needs analysis has simply been based on an informal conversation with company executives. This, in turn, requires the intelligence team to have a consultative approach, or at least the ability to negotiate productively with decision makers.

2. Coverage of secondary sources of information

As part of the information analysis cycle, we separately highlight the collection of information from secondary and primary sources. There are a number of reasons for this. First, collecting information from publicly available sources is less expensive than going directly to primary sources. Secondly, it is simpler, provided, of course, that the people tasked with this task have sufficient experience in studying available secondary sources. In fact, information source management and associated cost optimization are a separate area of expertise in themselves. Third, reaching out to secondary sources of information before conducting interview research will provide those conducting such research with valuable background information of a general nature that can be verified and used in response to information from interviewees. In addition, if during the study of secondary sources it is possible to obtain answers to some questions, this will reduce the cost of the primary source research stage, and sometimes even eliminate the need for them.

3. Primary Source Research

No matter how vast the amount of publicly available information is today, not all information can be accessed through the study of secondary sources. After examining secondary sources, gaps in the research can be filled by interviewing experts who are knowledgeable about the research topic. This stage can be relatively expensive compared to the study of secondary sources, which, of course, depends on the scale of the task at hand, as well as on what resources are involved: companies often involve third parties in participating in primary source research.

4. Analysis

After collecting information from various sources, it is necessary to understand what exactly is needed for an initial needs analysis in accordance with the task. Again, depending on the scope of the task at hand, this stage of research can be quite expensive, since it includes at least time expenditure of internal, and sometimes external, resources and, possibly, some additional verification of the correctness of the analysis results through further interview.

5. Delivery of results

The format for presenting results after completing the task of analyzing information is of no small importance for end users. Typically, decision makers do not have time to search for key insights from the large volume of data they receive. The main content needs to be translated into an easy-to-digest format keeping in mind their requirements. At the same time, additional background data should be readily available for those who become interested and want to dig deeper. These basic rules apply regardless of the format in which the information is presented, whether it is database software, a newsletter, a PowerPoint presentation, a face-to-face meeting, or a seminar. In addition, there is another reason why we separated the information delivery stage from the end use and receiving feedback and suggestions on the analytical information provided. Sometimes decisions will be made in the same sequence in which analytical information will be provided. However, more often than not, basic, reference materials will be provided before the actual decision situation arises, so the format, channel, and manner in which the information is presented influences how it is received.

6. Use and provision of comments/comments

The use phase serves as a litmus test for assessing the success of the information analysis task. It allows you to understand whether the results obtained meet the needs identified at the very beginning of the information analysis process. Regardless of whether all initial questions have been answered, during the use phase new questions and the need for new needs analysis typically arise, especially if the need for information analysis is ongoing. In addition, as a result of the joint efforts to create information materials between end users and information analysts, by the time it reaches the use stage, it may be that the end users of such information have already contributed to the expected end result. On the other hand, those who were primarily involved in the analysis may be actively involved in the process of drawing conclusions and interpreting the results on the basis of which final decisions will be made. Ideally, thoughtful observations and comments during the use phase can already be used as the basis for a needs assessment for the next information analysis task. Thus, the cycle of the information analysis process is completed.

Getting Started: Developing an Information Analysis Process

Determination of decision-making stages in business processes that require analytical market research

The term "decision analytics" has become increasingly popular as companies with existing analytics programs have begun to consider options to better integrate those programs into their decision-making processes. How abstract or concrete measures will be to “improve the connection between the final results of information analysis and business processes” will largely depend on whether these business processes have been formally defined, and also on whether the group has in information analysis, understanding the specific information needs associated with the decision-making stages of these processes.

As we mentioned in Chapter 1, the methods and techniques discussed in this book are best suited for companies that already have structured business processes, such as strategy development. Companies whose governance is less structured may need to be somewhat creative in using international market intelligence approaches to suit their existing governance arrangements. However, the basic principles we cover here will apply to any company.

Assessing information analytics needs: Why is it so important?

Given that understanding the key requirements for information analysis at the outset of the process has a greater impact on the quality of the final results than any other step in the process, it is striking that too little attention is often paid to the needs assessment phase. Despite the potential for resource limitations in other phases of the information analysis process, careful attention to needs assessment alone would in many cases greatly enhance the value and applicability of the end results of the process, thus justifying the investment of time and resources in the information analysis task. Below we look at specific ways to improve the quality of your needs assessment.

It is often automatically assumed that management knows what information the company needs. However, in reality, senior management typically has an understanding of only part of their organization's information needs, and even then may not be in the best position to determine exactly what information is needed, let alone where it is needed. can be found.

As a result, a situation is constantly repeated when, in order to perform information analysis tasks, there is neither a clearly formulated idea of the problem nor its business context. Those who are most familiar with information sources and analysis methods waste time processing seemingly haphazard data and are blind to the big picture and the approaches that make the most difference to the company. Unsurprisingly, the result is that decision makers receive far more information than they need, which is counterproductive because they soon begin to ignore not only useless information, but also important information. They do not need more information, but better and more accurate information.

At the same time, decision makers may have unrealistic expectations about the availability and accuracy of information because they did not consult with experts in the field of information analysis before setting the problem. Therefore, ideally, information analysts and decision makers should be in constant contact with each other and work together to ensure that both parties have the same understanding of priority information needs. The ability to manage this process will require a number of skills from analysts working in this direction:

- The analyst must understand how to identify and define the information needs of decision makers.

- The analyst must develop effective communication, interviewing and presentation skills.

- Ideally, the analyst should understand psychological personality types in order to take into account the different orientations of decision makers.

- The analyst must have knowledge of the organizational structure, culture and environment, as well as the key individuals being interviewed.

- The analyst must remain objective.

Work within the information analysis cycle and eliminate bottlenecks in the process

In the initial stages of implementing an information analysis program, the target group for the activities is usually limited, as well as the final results that the program produces. Similarly, when processing the final results, various difficulties (so-called “bottlenecks”) often arise: even simple collection of disparate data from secondary and primary sources may require knowledge and experience that the company does not have, and after completing the collection of information, it may be time-consuming and there are insufficient resources to conduct detailed analysis of the collected data, let alone produce informative and well-researched presentations that can be used by decision makers. Moreover, at the initial stages of developing an information analysis program, almost no company has special tools for storing and distributing the results of such analysis. Typically, the results are ultimately made available to target groups in the form of regular email attachments.

The complexities of performing an analytical task within the information analysis cycle can be described using the standard project management triangle, i.e., it is necessary to complete the task and produce the result under three main constraints: budget, deadlines and scope of work. In many cases, these three constraints compete with each other: in a standard information analysis task, an increase in the amount of work will require an increase in time and budget; a tight schedule will likely mean an increase in the budget and at the same time a reduction in the scope of work, and a limited budget will most likely mean both a limitation in the scope of work and a reduction in the time frame for the project.

The occurrence of bottlenecks in the information analysis process usually leads to significant friction in completing the research task within the information analysis cycle during the initial stages of developing a program for such analysis. Since resources are limited, the most critical bottlenecks should be addressed first. Is the intelligence team sufficiently equipped to carry it out? Is additional training necessary? Or is the problem rather that analysts lack valuable information to work with—in other words, the most critical bottleneck is information collection? Or maybe the information analysis group simply does not have enough time, that is, the group is not able to respond to urgent requests in a timely manner?

There are two ways to improve the efficiency of performing an analytical task within the information analysis cycle. The “throughput” of the cycle is the thoroughness with which the intelligence team can handle analytical tasks at each stage and the speed with which the question is answered. In Fig. Figure 2 shows the difference between these approaches and, in general, the difference between strategic analysis tasks and research requests that require a rapid response.

Although both approaches take the analytical task through all stages of the information analysis cycle, the information analysis team tasked with quickly conducting research will work on studying secondary and primary sources in parallel (sometimes one phone call to an expert can provide the necessary answers to the questions posed in the research request). In addition, in many cases the analysis and presentation of information are combined, for example, in a summary that the analyst passes on to the manager who requested the information.

Intelligence cycle performance can be improved by adding either internal (hired) or external (acquired) resources where they are needed, resulting in better results and increased ability to serve more and more user groups within the organization.

The same principle applies to ensuring speed in the implementation of a sequence of operations, that is, what matters is how quickly an urgent research task moves through the various stages of the cycle. Traditionally, companies have primarily focused on ensuring stable capacity through long-term resource planning and staff training schemes. However, with the development of such a specialized area as information analysis, and the increasing availability of global professional resources attracted from outside, temporary schemes that are implemented in each specific case and provide the necessary flexibility are becoming increasingly widespread.

In Fig. Figure 3 shows the two types of outputs of the information analysis cycle, that is, strategic analysis and research requiring rapid response (see the graph of the outputs of information analysis). Despite the fact that tasks for conducting research that require rapid response are usually associated with business processes, the level of their analysis is not very high due to the banal lack of time to conduct such analysis. On the other hand, strategic analysis tasks tend to involve a high level of co-creation during the analysis and information delivery phase, which places them almost at the apex of the triangle where the information obtained is interpreted and applied.

Continuous development: striving for an international level of information analysis